Why Your Broker's Regulation Tier Matters More Than You Think

Not all forex broker regulation provides the same level of protection. The jurisdiction behind a broker's licence determines whether your funds are segregated, what compensation you can claim if things go wrong, and whether you have any meaningful recourse at all.

Most traders spend more time picking an entry strategy than checking who actually regulates their broker. That is understandable. Regulation is unglamorous. But it is also one of the few things that genuinely separates brokers operating under serious oversight from those operating with very little.

This guide breaks down what regulatory tiers actually mean in practice, which regulators carry the most weight, and what to look for before you deposit.

What Is Forex Broker Regulation?

Forex broker regulation is the legal framework under which a broker is authorised to operate. A regulated broker must:

- Meet specific capital requirements

- Keep client funds segregated from company funds

- Submit to regular audits

- Follow conduct rules set by the overseeing authority

Regulation creates a framework of enforceable rules and, in many jurisdictions, a compensation scheme that activates if a regulated firm fails. It does not guarantee profits, prevent losses, or eliminate the possibility of broker insolvency.

The practical difference between a well-regulated broker and a loosely regulated one is not always visible during normal trading conditions. It tends to become very visible when something goes wrong.

Pick a well-regulated CFD provider among the best forex & CFD brokers.

The Concept of Regulatory Tiers

The tier framework used in this article is an editorial convention, not an official classification system. No global body ranks regulators on a numbered scale. The groupings here reflect commonly observed differences in regulatory stringency, enforcement history, and client protection infrastructure.

Tier 1 covers regulators in major financial centres with robust oversight, strong enforcement records, and meaningful compensation schemes.

Tier 2 covers regulators with credible frameworks and reasonable client protections, though often with lower capital requirements or narrower compensation coverage.

Tier 3 covers offshore and lightly regulated jurisdictions where oversight is minimal, compensation schemes are rare, and legal recourse is limited.

These are useful reference points, not absolute verdicts. A broker regulated in a Tier 2 jurisdiction is not automatically suspect. Context matters.

Tier 1 Regulators: The Strongest Frameworks

FCA (Financial Conduct Authority): United Kingdom

The FCA is widely regarded as one of the most rigorous retail financial regulators in the world. Brokers authorised by the FCA must maintain minimum capital requirements, segregate client funds, and comply with detailed conduct of business rules.

UK retail clients benefit from coverage under the Financial Services Compensation Scheme (FSCS), which covers eligible claims up to £85,000 for investment firm failures. Negative balance protection applies to retail clients trading CFDs and rolling spot forex, meaning losses cannot exceed the funds in the account.

Note: The FSCS deposit protection limit was raised to £120,000 in December 2025, but this applies to bank deposits only. The investment firm compensation limit remains £85,000.

Following Brexit, FCA regulation no longer provides passporting rights into the EU. EU-based clients trading with FCA-regulated brokers should verify how their accounts are structured and which entity actually holds their funds.

ASIC (Australian Securities and Investments Commission): Australia

ASIC operates a well-regarded framework with meaningful capital and conduct requirements. Australian Financial Services (AFS) licence holders must maintain client money in segregated accounts and comply with dispute resolution obligations.

Compensation in Australia works differently to the UK. Australia does not have a direct equivalent to the FSCS. The Compensation Scheme of Last Resort (CSLR) exists but has a limited scope, covering:

- Personal financial advice

- Credit intermediation

- Securities dealing

- Credit provision

The coverage ceiling is AUD $150,000 per eligible claim (approximately £77,000–£80,000 at current rates), which is lower than the FSCS investment firm limit. Traders relying on Australian regulation should understand that compensation arrangements are not equivalent to those available under FCA authorisation.

ASIC has tightened leverage limits for retail clients in recent years, broadly aligning with the direction taken by European regulators.

CFTC/NFA (Commodity Futures Trading Commission / National Futures Association): United States

The US framework for retail forex trading is among the most restrictive in the world. The CFTC and NFA impose:

- Strict capital requirements

- Leverage caps (50:1 maximum on major currency pairs for retail clients, per 17 CFR Part 5)

- Rigorous reporting obligations on registered firms

The Securities Investor Protection Corporation (SIPC) does not cover forex trading accounts. As SIPC's own guidance confirms, retail forex accounts in the US sit outside SIPC protection. The regulatory strength here comes from structural oversight and enforcement rather than a broad compensation scheme.

The US framework effectively limits access to foreign brokers. Americans are largely restricted to trading with CFTC-registered firms, which is a deliberate design choice rather than an oversight.

Tier 2 Regulators: Credible but More Variable

CySEC (Cyprus Securities and Exchange Commission): Cyprus

CySEC is an EU member-state regulator that gained significant prominence as a licensing hub for brokers serving European retail clients. Regulated entities are subject to MiFID II requirements, which include:

- Leverage limits for retail clients trading CFDs and rolling spot forex

- Negative balance protection

- Best execution obligations

Retail clients of CySEC-regulated firms are eligible for coverage under the Investor Compensation Fund (ICF), up to €20,000 per eligible claimant (the lower of 90% of the total claim or €20,000). This is meaningfully lower than the FSCS limit and is worth factoring in when comparing brokers.

Post-Brexit, CySEC regulation no longer provides passporting access to UK clients in the same way. UK traders dealing with CySEC-regulated entities should confirm whether they are being served by a UK-authorised entity or an EU-based one, as this determines which regulatory protections apply.

CySEC has strengthened its enforcement posture in recent years, though it has historically been viewed as more accommodating than the FCA or ASIC in certain areas of conduct oversight.

Other Notable Tier 2 Regulators

BaFin (Germany): A rigorous regulator within the EU framework, with strong consumer protection standards and MiFID II compliance. Germany's domestic supervision is considered thorough.

AMF (France): The Autorité des Marchés Financiers oversees French financial markets with a detailed conduct framework and EU-aligned investor protections.

FINMA (Switzerland): Switzerland sits outside the EU but maintains a well-regarded regulatory regime. FINMA oversight is strict, though the domestic focus means fewer retail forex brokers operate under this licence.

DFSA (Dubai): The Dubai Financial Services Authority operates within the DIFC free zone and maintains a relatively rigorous framework by regional standards. Appropriate for traders dealing with DIFC-based entities, but distinct from the broader UAE regulatory environment.

MAS (Singapore): The Monetary Authority of Singapore runs a well-structured licensing regime. Capital requirements are meaningful, and conduct standards are taken seriously. MAS-regulated brokers serving retail clients operate within a credible framework.

Tier 3 Regulators: Proceed with Caution

Tier 3 jurisdictions include offshore locations such as Vanuatu, the Seychelles, Belize, and similar centres where licensing is relatively accessible, capital requirements are low, and enforcement infrastructure is limited.

This does not mean every broker licensed in these jurisdictions is fraudulent. Some operate legitimately and use offshore licensing for cost or flexibility reasons. The structural protections available to traders are, however, materially weaker.

Key concerns with Tier 3 jurisdictions:

- Compensation schemes are either absent or nominal

- Segregation requirements vary significantly

- Legal recourse in the event of a dispute is often impractical for retail traders operating from another country

- Regulatory action is rare, and enforcement outcomes are difficult to achieve from overseas

For most retail traders, a Tier 3 licence should prompt further scrutiny before any funds are deposited.

What Segregated Funds Actually Mean

Fund segregation means a broker must hold client money in accounts that are separate from the firm's own operating funds. If the broker becomes insolvent, client funds should not be accessible to creditors settling business debts.

In practice, segregation requirements vary in their specifics. Some regulators require funds to be held in named trust accounts at approved institutions. Others set less prescriptive rules. The quality of segregation as a protection depends on how the requirement is written and how rigorously it is enforced.

Segregation reduces risk but does not eliminate it. In complex insolvencies, the process of recovering client funds can take time and may not be complete.

Leverage Limits and What They Signal

Leverage caps attract less attention than compensation schemes, but they reflect something important about a regulator's attitude toward retail client protection.

The FCA, ASIC, ESMA-aligned regulators, and the CFTC have all imposed leverage limits for retail clients in recent years. The reasoning is consistent: excessive leverage is the primary mechanism through which retail traders suffer rapid, large losses.

A broker offering 500:1 leverage to retail traders is almost certainly operating under a framework with minimal consumer protection requirements. High leverage availability is frequently an indicator of regulatory tier, not a feature to seek out.

How to Check a Broker's Regulation

Checking a broker's regulation takes around five minutes and is worth doing before any deposit.

Each major regulator maintains a public register of authorised firms. Search the FCA register, ASIC's professional registers, or the NFA's background affiliation status information centre (BASIC) directly. Do not rely on information displayed on a broker's own website as the sole source of verification.

Key things to confirm:

- The entity name on the licence matches the entity you are opening an account with

- The licence status is current and active

- The licence type covers the products you intend to trade

- The jurisdiction of the licence matches where your account is being held

Some brokers operate multiple entities under different licences in different jurisdictions. Which entity your account sits under determines which protections apply to you.

Questions to Ask Before You Deposit

Before funding any account, run through these five questions. Clear answers should take only a few minutes to find. A broker that makes this information difficult to locate is telling you something worth knowing.

- Which legal entity am I opening an account with, and which regulator covers that entity?

- Where will my funds be held, and in what type of account?

- What compensation scheme applies to my account, and what is the coverage limit?

- What leverage limits apply to retail clients under this licence?

- Is there a formal dispute resolution process, and which body oversees it?

Frequently Asked Questions

Does regulation guarantee my money is safe?

No. Regulation creates a framework of rules and oversight, and in many jurisdictions provides a compensation scheme if a firm fails. It does not eliminate risk or guarantee the return of funds in all circumstances.

Is an offshore broker always a bad choice?

Not automatically. Some offshore-licensed brokers operate responsibly. The issue is that the structural protections available to traders are materially weaker, and recourse in the event of a problem is much harder to pursue.

What is the difference between the FCA and CySEC for retail clients?

Both operate under credible frameworks, but the FCA's compensation ceiling for investment firm failures (£85,000 via the FSCS) is substantially higher than CySEC's ICF limit (€20,000). Enforcement records and conduct oversight standards also differ.

Can I trade with a US broker if I live outside the US?

Most CFTC-registered brokers do not accept clients from outside the United States. The US framework is largely domestic by design.

What does negative balance protection mean?

It means retail clients cannot lose more than the funds they have deposited. If a trade moves against them beyond their account balance, the broker absorbs the loss rather than pursuing the client for additional funds. This protection applies to retail clients trading CFDs and rolling spot forex under FCA and MiFID II-aligned regulation. It does not typically apply to professional clients.

How do I verify a broker's licence?

Check the regulator's own public register directly, using the broker's legal entity name. Do not rely solely on claims made on the broker's website.

About the authors

Related articles

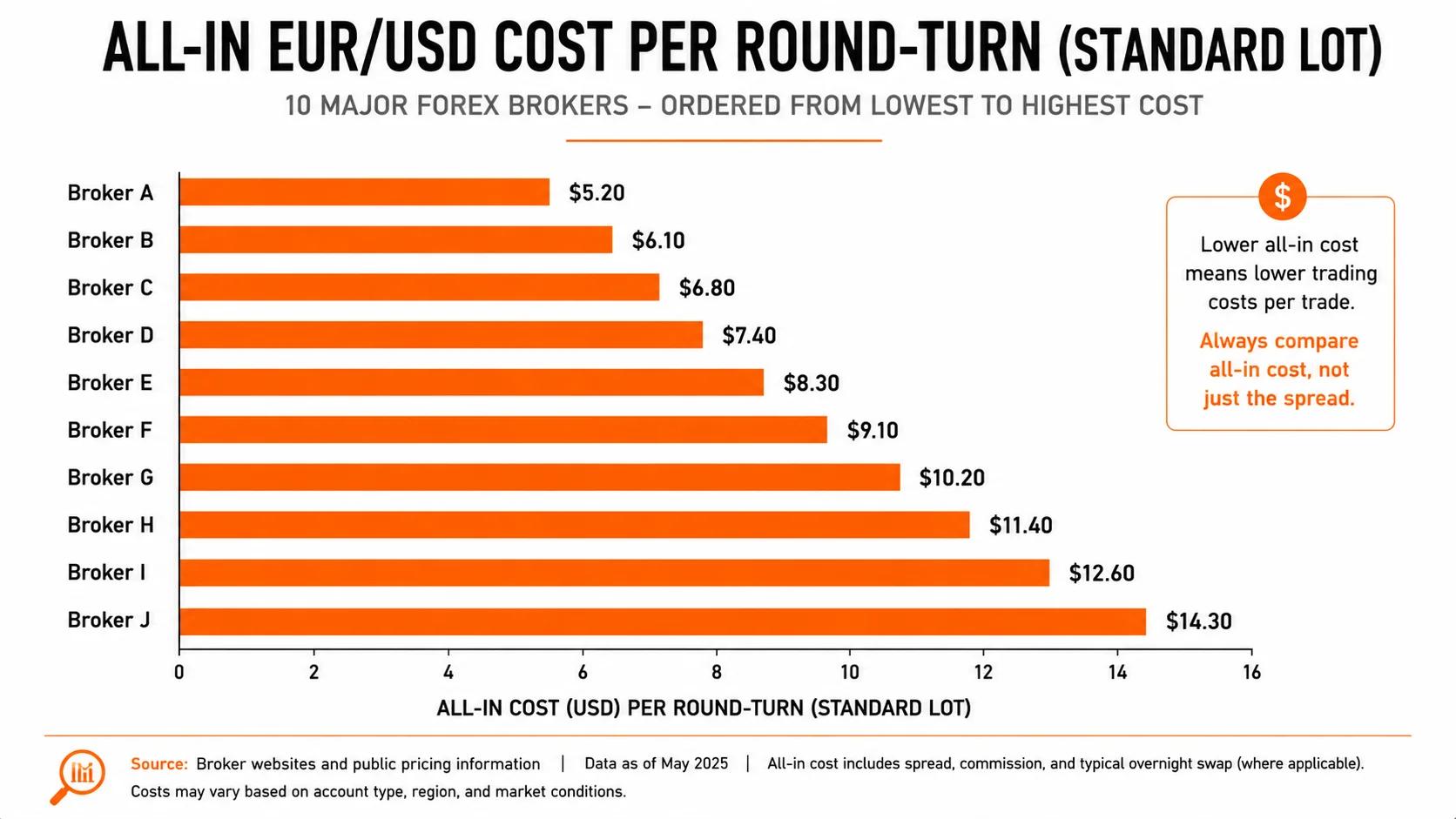

The True Cost of Trading: A Data-Driven Comparison Across 10 Forex Brokers

Full-cost comparison across spreads, commissions, swap rates, and fees for 10 major forex brokers; including EUR/USD, GBP/USD, and Gold trading costs per lot.

7 Moments to Be Bullish on Gold (When to Buy Gold and Why It Matters)

Discover 7 key moments that signal when to buy gold, from real rate shifts to dollar weakness and central bank demand.

Best Day Trading Platforms: Features, Fees, and Execution Speed Compared

A structured comparison of the best day trading platforms: execution latency, spreads, FCA leverage caps, tax reporting, and the psychological tooling that separates disciplined traders from

0 comments