Why Offshore Forex Brokers Keep Winning Despite the Risks

Offshore forex brokers carry real risks that regulators are happy to spell out in detail. So why are millions of traders still using them, and why does that number keep growing? This article explains the structural reasons behind offshore brokers' appeal, what you give up by using one, and how to make a genuinely informed decision.

What Makes a Broker "Offshore"

The word "offshore" gets used as a vague catch-all, which makes it nearly useless without context. To understand the trade-off, you need to understand what it actually means structurally.

Jurisdiction Matters More Than You Think

A broker is "offshore" relative to you: it is licensed and regulated in a jurisdiction that is not your home country, and usually one with a lighter regulatory framework than major financial centers. The broker operates legally under its local rules. Whether it operates legally for you depends on your country's laws, which vary considerably.

A broker regulated in the UK operates under FCA rules regardless of where you are. A broker licensed in St. Vincent and the Grenadines operates under SVG rules, which differ in ways that have direct consequences for your funds.

Note: The legal status of using an offshore broker depends on your local jurisdiction. This varies by country and is worth verifying before you deposit.

Common Offshore Hubs and What They Offer

Several jurisdictions have become common bases for offshore brokers operating in the forex space. The most frequently encountered include:

- St. Vincent and the Grenadines (SVG): SVG has historically been popular due to its minimal requirements for forex operators. Following a 2023 FSA circular, SVG-incorporated forex operators are now expected to demonstrate existing licensure in another jurisdiction, though enforcement remains limited and the framework is substantially lighter than any top-tier regulator.

- Seychelles: Has a financial regulator (FSA Seychelles) with licensing requirements, but substantially lower capital and operational standards than major regulators.

- Vanuatu: The Vanuatu Financial Services Commission licenses forex brokers. Requirements exist but are lighter than FCA, ASIC, or similar bodies.

- Belize: The International Financial Services Commission regulates forex entities, within a lighter-touch framework compared to top-tier jurisdictions.

Each hub has its own rules. Lumping them together as equally risky or equally reliable misrepresents what you are actually dealing with.

The Regulatory Gap: What Offshore Means in Practice

Regulatory warnings tend to describe offshore brokers as uniformly dangerous. Offshore broker marketing tends to describe regulation as bureaucratic noise. Neither is the full picture. The honest version sits somewhere between them.

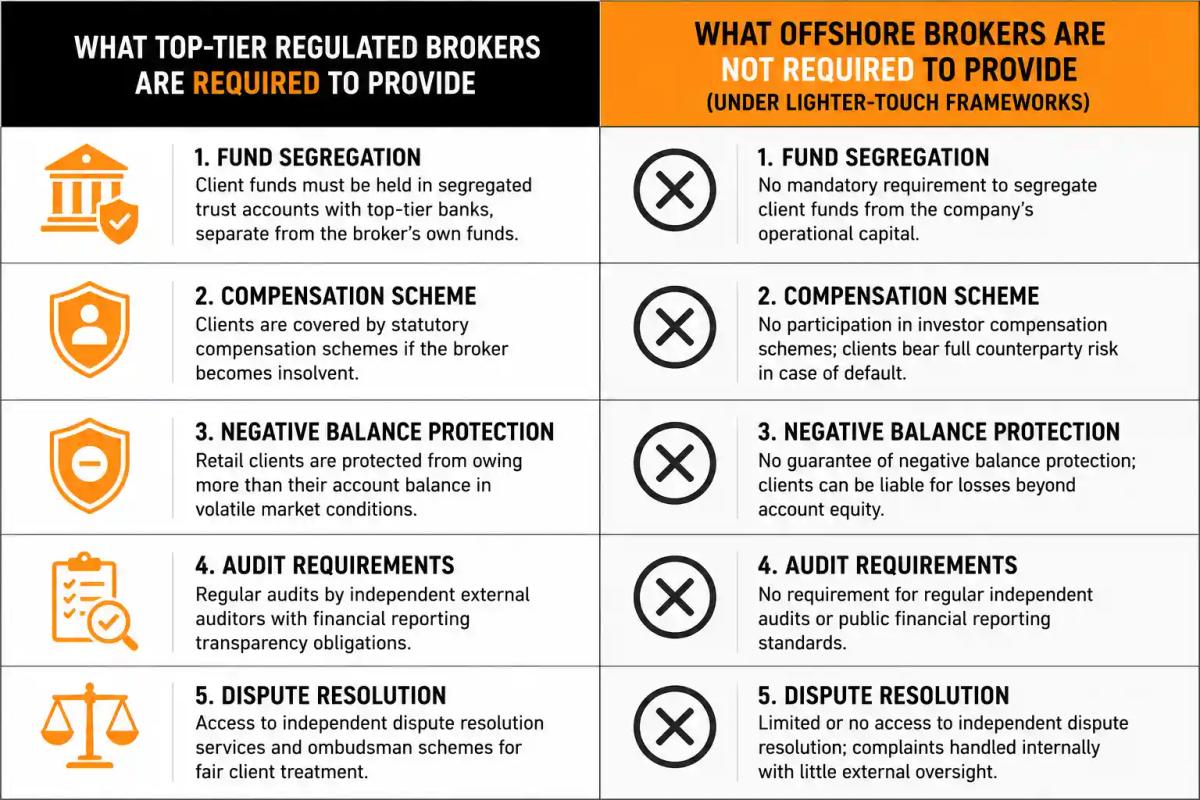

What Offshore Brokers Are Not Required to Do

Depending on the jurisdiction, offshore brokers may not be required to:

- Segregate client funds from company operating funds

- Maintain minimum capital reserves that protect clients if the firm becomes insolvent

- Participate in any compensation scheme

- Provide negative balance protection

- Follow leverage limits imposed by regulators like the FCA, ASIC, or CFTC/NFA

- Submit to routine audits of financial practices

- Follow formal dispute resolution processes with an independent ombudsman

Each item has direct implications for what happens to your money if something goes wrong.

What Legitimate Offshore Brokers Do Anyway

This is where it gets more nuanced. Many established offshore brokers voluntarily adopt practices beyond their regulatory minimums but because reputation is a competitive asset in a crowded market.

A broker that has operated for ten or more years with a track record of smooth withdrawals and no major client fund issues has something to lose. That creates a market incentive to behave responsibly that, while not equivalent to regulatory enforcement, is not negligible either.

The distinction worth making is between brokers that operate offshore as a deliberate choice within a sustainable business model, and those that use light-touch jurisdictions specifically to limit accountability. The two can look identical from the outside until, suddenly, they do not. More on that below.

Why Traders Choose Offshore Brokers

This is the part most broker-risk articles skip over, which is exactly why those articles rarely change anyone's behavior.

Leverage Limits and Why Regulated Markets Cap Them

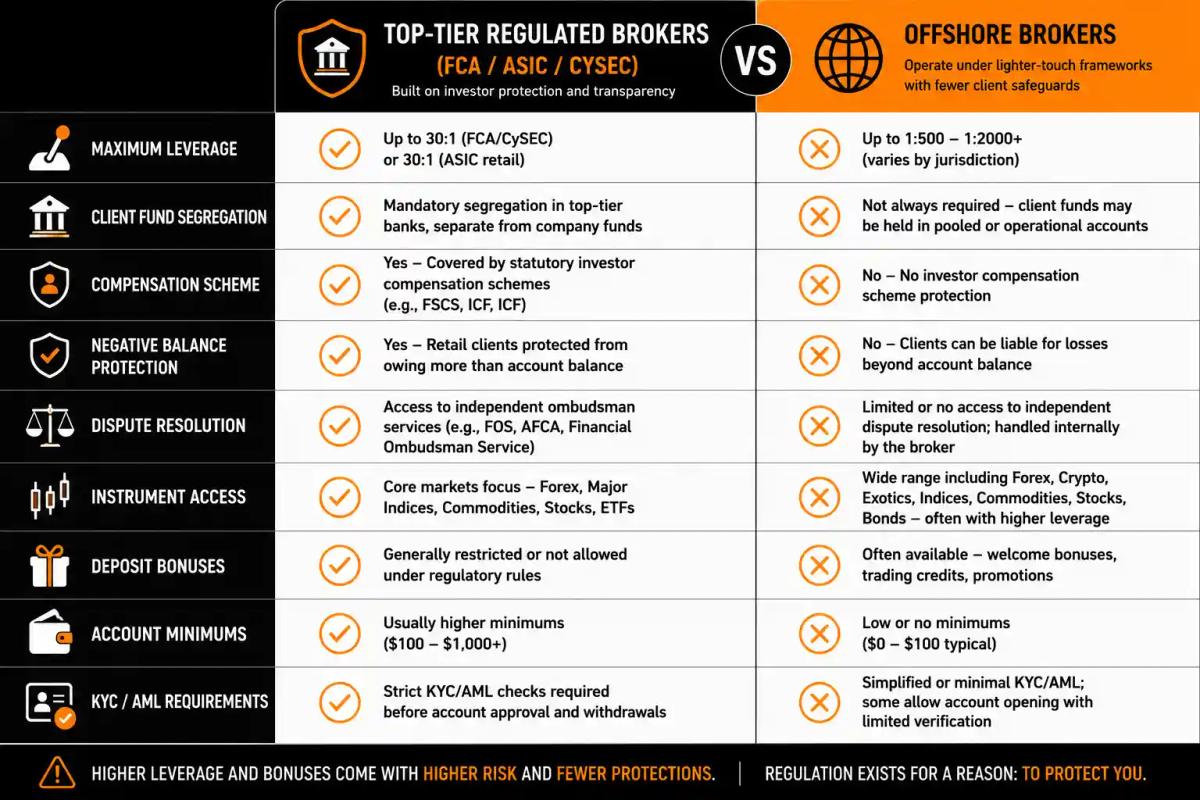

Leverage is the most cited reason. The FCA's permanent retail leverage caps, established under PS19/18, limit retail clients to 30:1 on major forex pairs. CySEC applies equivalent limits under its own implementation of the same framework. ASIC in Australia applies similar restrictions under its product intervention rules.

Offshore brokers routinely offer substantially higher leverage, commonly in the range of 200:1 to 500:1 or beyond. For a trader who believes they can manage their own position sizing, the leverage ceiling in regulated markets is genuinely restrictive.

The trade-off is worth stating directly: leverage amplifies losses at exactly the same rate it amplifies gains. A high-leverage account does not make you more likely to profit. A small adverse move on your full exposure can be sufficient to wipe your margin. Offshore brokers offer more rope, not a different kind of rope.

Access to Instruments and Markets Not Available Locally

Some traders turn to offshore brokers not for leverage but for access. Regulated retail brokers in major jurisdictions have progressively restricted the range of available instruments. Certain CFDs, crypto derivatives, exotic pairs, and alternative markets may not be accessible through an FCA or CySEC-regulated retail account.

Offshore brokers frequently offer a wider product range. For a trader with a specific strategy that requires instruments unavailable locally, the offshore broker may be the only functional option.

Lower Account Minimums and Fewer Restrictions

Many offshore brokers accept accounts from low minimum deposits, with fewer identity verification hurdles than major regulated firms. For traders in countries where the KYC process at tier-one regulated brokers is genuinely burdensome, this is a practical advantage rather than a signal of fraud.

Offshore accounts also tend to impose fewer restrictions on trading strategy. Scalping, hedging, and EA-based strategies that are limited or prohibited on some regulated platforms are often permitted without restriction.

The Bonus and Promotion Factor

The FCA prohibits regulated firms from offering deposit bonuses to retail clients under its permanent conduct rules. CySEC applies equivalent prohibitions. Offshore brokers are not bound by these restrictions. Deposit bonuses, cashback schemes, and promotional offers are freely used. Every experienced trader knows that bonus terms involve conditions that can complicate withdrawals, but the promotional economics can still appeal to traders who know how to navigate them.

The Real Risks, Laid Out Without Theatrics

Here is a clear-eyed account of what can actually go wrong.

No Compensation Scheme If the Firm Fails

If an FCA-regulated broker becomes insolvent, eligible clients may be able to claim through the FSCS up to £85,000. No equivalent exists with offshore brokers.

If your offshore broker becomes insolvent, your client balance becomes a creditor claim in a foreign jurisdiction. In practice, recovery is rare and partial at best.

Dispute Resolution Is Your Problem

With a regulated broker, a formal complaints process exists. If the broker does not resolve your complaint, you can escalate to an independent ombudsman with real authority to compel resolution.

With an offshore broker, your leverage in any dispute is limited to the broker's willingness to cooperate. Legal action across jurisdictions is expensive, slow, and uncertain. Your practical options narrow considerably.

Withdrawal Issues and How to Spot Red Flags Early

Withdrawal problems are the most common practical issue traders report with offshore brokers. These include:

- Unexpected verification requests that arise only when a withdrawal is submitted

- Delays that extend from days into weeks without clear explanation

- Bonus terms invoked to restrict withdrawal of profitable trading gains

- Documentation requests that escalate without resolution

Red flags to watch before problems develop:

- Withdrawal processing times not clearly stated on the site

- No verifiable business address or contact information beyond a web form

- Reviews that mention smooth deposits but difficult withdrawals

- Bonus offers with vague or unavailable terms and conditions

- No clear regulatory license number, or one that cannot be verified on the licensing authority's public register

Who Offshore Brokers Actually Suit

Being direct about this is more useful than a blanket warning, and more honest than a blanket endorsement.

Experienced Traders Who Understand the Trade-Off

An experienced trader with a structured risk management approach, a clear position sizing strategy, and enough capital to maintain discipline regardless of available leverage is in a genuinely different position than a new trader who opens a high-leverage account simply because it was on offer.

If you know exactly why you want higher leverage or specific instrument access, understand what protection you are forfeiting, and are keeping only a working capital allocation with an offshore broker rather than your total trading capital, the risk profile is meaningfully different from what it might look like from the outside.

Traders in Restricted Jurisdictions With Limited Regulated Options

Some traders have no practical access to tier-one regulated brokers. Those brokers may not accept clients from their country, local regulatory restrictions may make available products too limited to trade their strategy, or the domestic regulatory environment itself may be less reliable than a well-established offshore alternative.

For these traders, the choice is often between offshore brokers and not trading in any functional way. That context matters when evaluating the decision.

How to Reduce Risk If You Use an Offshore Broker

This section is practical guidance for traders who are going to use offshore brokers. That is a more honest and useful starting point than pretending the previous sections will change everyone's mind.

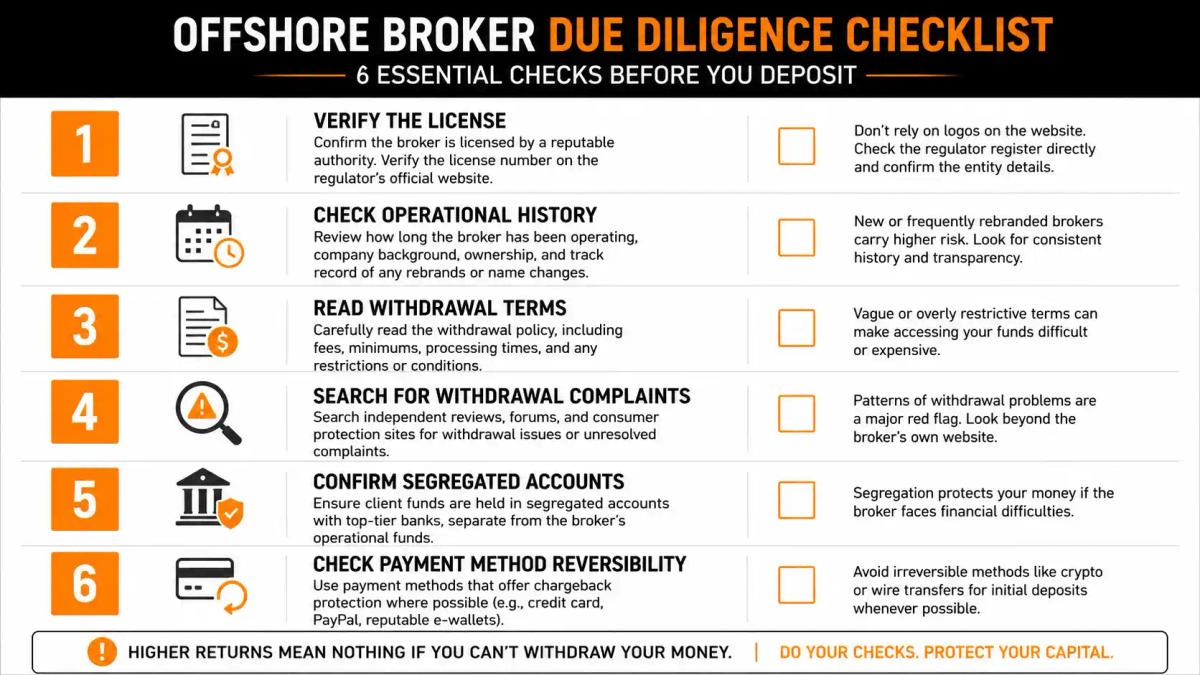

Due Diligence Checklist Before Depositing

- Verify the license exists. Look up the broker's stated license number directly on the licensing authority's public register. If it is not there, stop.

- Check operational history. How long has the broker been operating under its current name and ownership? Newer entities carry more risk.

- Read the withdrawal terms before depositing. Specifically check processing times, fees, verification requirements, and any conditions attached to bonuses.

- Search for withdrawal complaints. Look for specific accounts of withdrawal experiences on trader forums and review platforms. These are more informative than star ratings.

- Confirm segregated accounts. Some offshore brokers voluntarily offer segregated client fund accounts. Confirm in writing whether this applies to your funds.

- Check payment method reversibility. Depositing via a method with chargeback rights gives you one additional option if withdrawal problems arise.

Deposit Management and Withdrawal Testing

- Start with a minimal deposit that you are willing to lose entirely. This is the correct risk framing for any offshore broker relationship, not pessimism.

- Before depositing meaningful capital, complete at least one withdrawal to confirm the process works as described. Withdraw a small amount, note the timeline, and compare it to the stated terms.

- Never concentrate significant capital with a single offshore broker. If something goes wrong with an unregulated or lightly regulated entity, your exposure should reflect that risk.

- Withdraw profits regularly. Keeping large balances with an offshore broker increases your exposure to scenarios you cannot control.

Frequently Asked Questions

Is it legal to use an offshore forex broker?

It depends entirely on your country of residence. In many jurisdictions, using an offshore broker is not prohibited for individual traders, but some countries explicitly restrict or prohibit their residents from using unlicensed foreign financial services firms. You should verify the rules in your specific jurisdiction before depositing. This article cannot answer that question universally.

What happens to your funds if an offshore broker becomes insolvent?

If client funds are not segregated, which is not guaranteed under most offshore licenses, they can become part of the general estate in insolvency proceedings. Recovery through foreign legal systems is possible but typically slow, expensive, and partial. There is no compensation scheme that would cover your balance as a protected claim.

How do you tell a legitimate offshore broker from a fraudulent one?

The most reliable signals are: A verifiable license number on the licensing authority's public registerDocumented operational history of at least several yearsIndependently sourced evidence of successful withdrawals from real clientsClear and published terms on withdrawals and bonusesA functioning customer service channel with a real business address Fraudulent operations tend to have shorter histories and more inconsistencies in basic verifiable facts.

Is high leverage from an offshore broker actually an advantage for most traders?

For a small number of experienced traders with disciplined position sizing, access to higher leverage provides genuine strategic flexibility. For most retail traders, higher available leverage correlates with faster capital loss rather than improved returns. The leverage itself is neutral. The risk is in how it is used. If your edge does not require high leverage to work, a 500:1 option is less an advantage and more an additional risk to manage.

What is the difference between an offshore broker and an unregulated broker?

The terms overlap but are not identical. An offshore broker is based in a foreign jurisdiction and may or may not be regulated there. A broker licensed by the Vanuatu Financial Services Commission is technically offshore but regulated. A broker incorporated in SVG with no forex license is both offshore and unregulated. The risk profiles differ meaningfully. Unregulated brokers operate with no formal oversight at all. Offshore-but-regulated brokers operate under lighter-touch oversight. Both sit below top-tier regulated status, but they are not the same category of risk.

About the authors

Related articles

The True Cost of Trading: A Data-Driven Comparison Across 10 Forex Brokers

Full-cost comparison across spreads, commissions, swap rates, and fees for 10 major forex brokers; including EUR/USD, GBP/USD, and Gold trading costs per lot.

7 Moments to Be Bullish on Gold (When to Buy Gold and Why It Matters)

Discover 7 key moments that signal when to buy gold, from real rate shifts to dollar weakness and central bank demand.

Best Day Trading Platforms: Features, Fees, and Execution Speed Compared

A structured comparison of the best day trading platforms: execution latency, spreads, FCA leverage caps, tax reporting, and the psychological tooling that separates disciplined traders from

0 comments