Why Tight Spreads Are No Longer Enough to Judge a Forex Broker

Tight spreads became the headline metric in forex broker marketing, and for a while, that made sense. But the spread you see on the ticket is only one part of what you actually pay per trade, and for many traders, it is not even the biggest part.

This guide breaks down forex broker execution quality as a complete evaluation framework, so you can stop comparing spread columns and start comparing what actually affects your bottom line.

The Spread War and How It Distorted Broker Evaluation

How Zero-Spread Marketing Became the Industry Default

At some point in the last decade, forex brokers collectively decided that "0.0 pip spreads" was the most powerful thing they could put in a headline. One broker launched it, the next matched it, and within a few years the entire retail forex industry had raced to the bottom on advertised spreads. Today, you can find a dozen brokers claiming near-zero spreads on majors without much effort.

The problem is that zero-spread marketing is, at best, a partial truth. Those accounts typically charge a commission per lot. The spread gets shifted into a line item that looks different but costs the same, or more. Brokers that do offer genuinely tight spreads often offset the economics elsewhere in the execution chain, in ways that never surface in the marketing material.

The spread war made trading costs harder to see. A convenient outcome, as it happens, for any broker with mediocre execution.

What Traders Were Led to Believe (and What They Actually Got)

The implicit promise of tight spread marketing was simple: lower spread equals lower cost equals better results. That logic is clean and intuitive, but it does not hold up in practice.

What intermediate traders discovered in live conditions was a gap between advertised pricing and actual fills. Open a position during a busy news window and the fill can be several pips off the quoted price. Try to close a scalp in a fast market and get a requote. Compare end-of-month costs against what the spread alone would predict, and the numbers do not match.

That gap has a name: execution quality. It is what most broker comparison content does not discuss, because it is harder to turn into a comparison table.

What Execution Quality Actually Means

Execution quality is not a single number. It is a composite of several factors that together determine how closely your filled price matches your intended price, and how reliably that happens across market conditions.

Fill Speed and Latency

Fill speed is how quickly your order is processed and confirmed after you submit it. Measured in milliseconds, latency matters most when markets are moving. A 50ms delay in a calm market is invisible. The same delay during a rate decision can mean your fill is several pips away from where you clicked.

Brokers with infrastructure closer to major liquidity hubs tend to offer consistently lower latency. If your broker's servers are routed through a data centre far from major market infrastructure, that extra round-trip time shows up in your fills when it matters most.

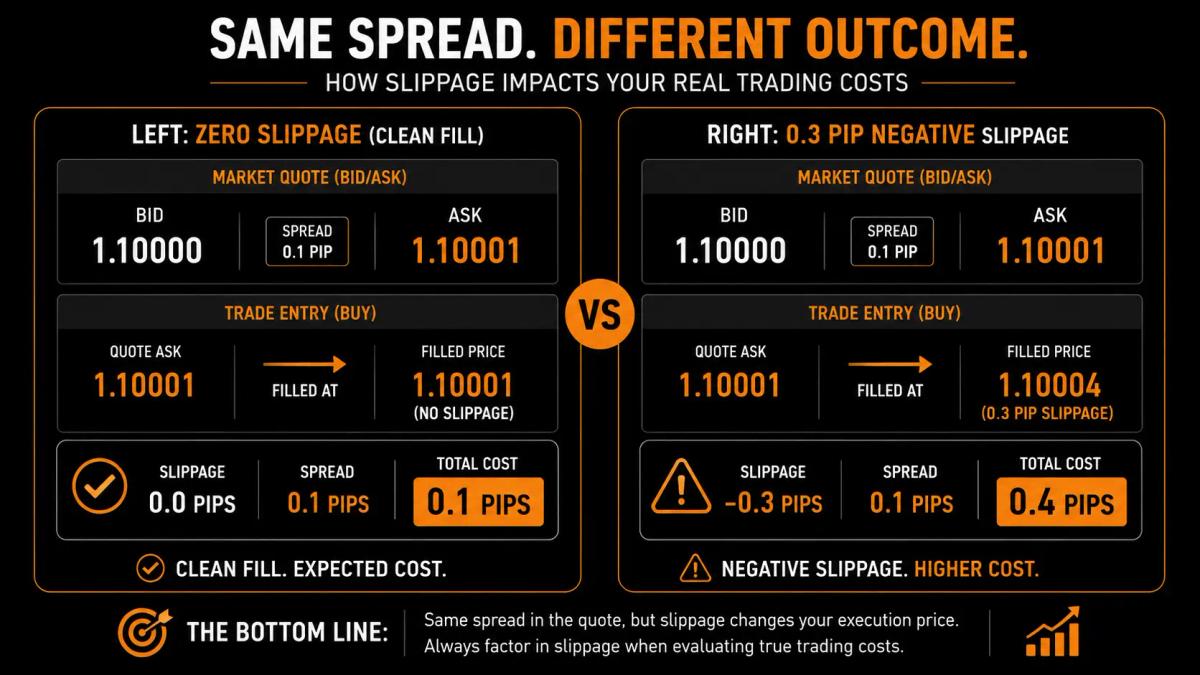

Slippage: Positive and Negative

Slippage is the difference between the price you requested and the price you received. It moves in both directions.

- Negative slippage means you got a worse price than requested: you bought higher or sold lower than intended.

- Positive slippage means the opposite. The market moved in your favour between order submission and fill, and you received a better price.

Both happen in live trading. What distinguishes brokers is the distribution and frequency of each. A broker with genuinely good execution passes positive slippage to clients.

A pattern that regulators and traders have raised as a concern is asymmetric slippage: fills at the requested price when the move is favourable, but slippage when it is not. If slippage consistently runs in one direction across your own trading records, that distribution is worth examining closely.

Requotes and Order Rejection Rates

A requote is when the broker cannot fill your order at the requested price and comes back with a new quote for you to accept or reject. In slow markets, requotes are rare. In fast markets, exactly when you want clean execution, they become a real problem.

Order rejection is the harder version: your order simply does not get filled at all. Rejection rates are not published by most brokers, but you can track them yourself. If you are submitting market orders and seeing rejections or consistent requotes during periods of moderate volatility, that is execution infrastructure failing at its core job.

Liquidity Depth and Price Stability

Price stability refers to how tightly your broker can hold quoted prices before having to reprice. A broker connected to deep, diverse liquidity across multiple tier-1 banks and non-bank liquidity providers can absorb order flow without repricing as frequently. A broker with thin liquidity or a single provider shows wider, less stable prices when volume spikes.

For most retail traders on most days, liquidity depth is invisible. During high-impact events, it is everything.

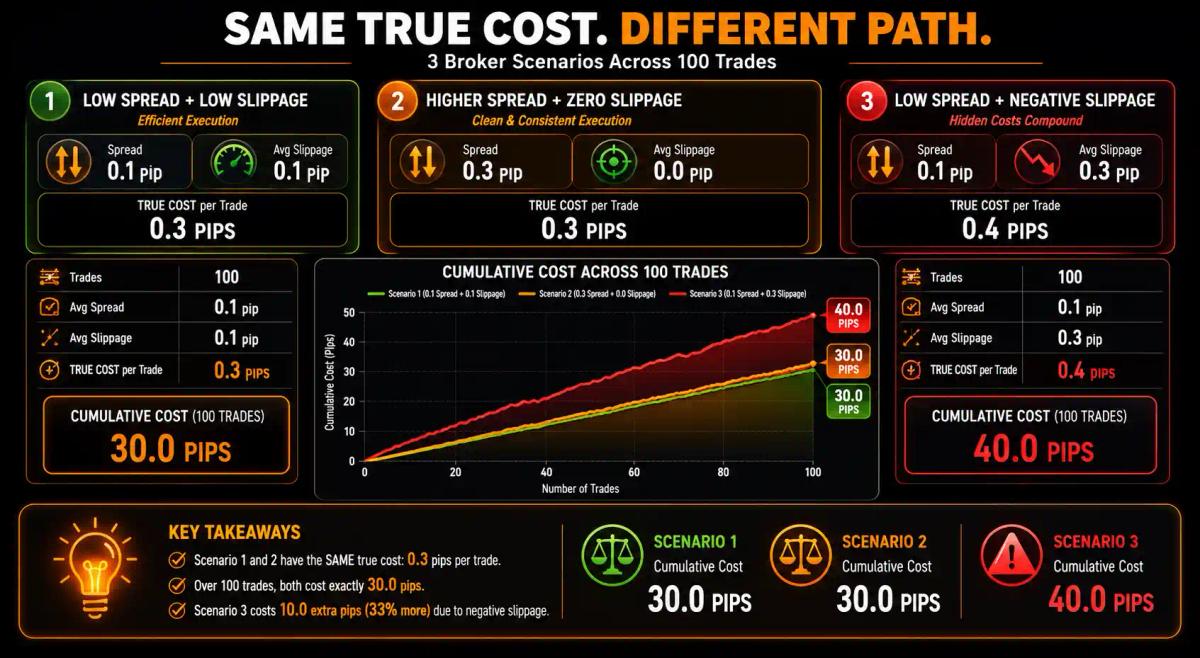

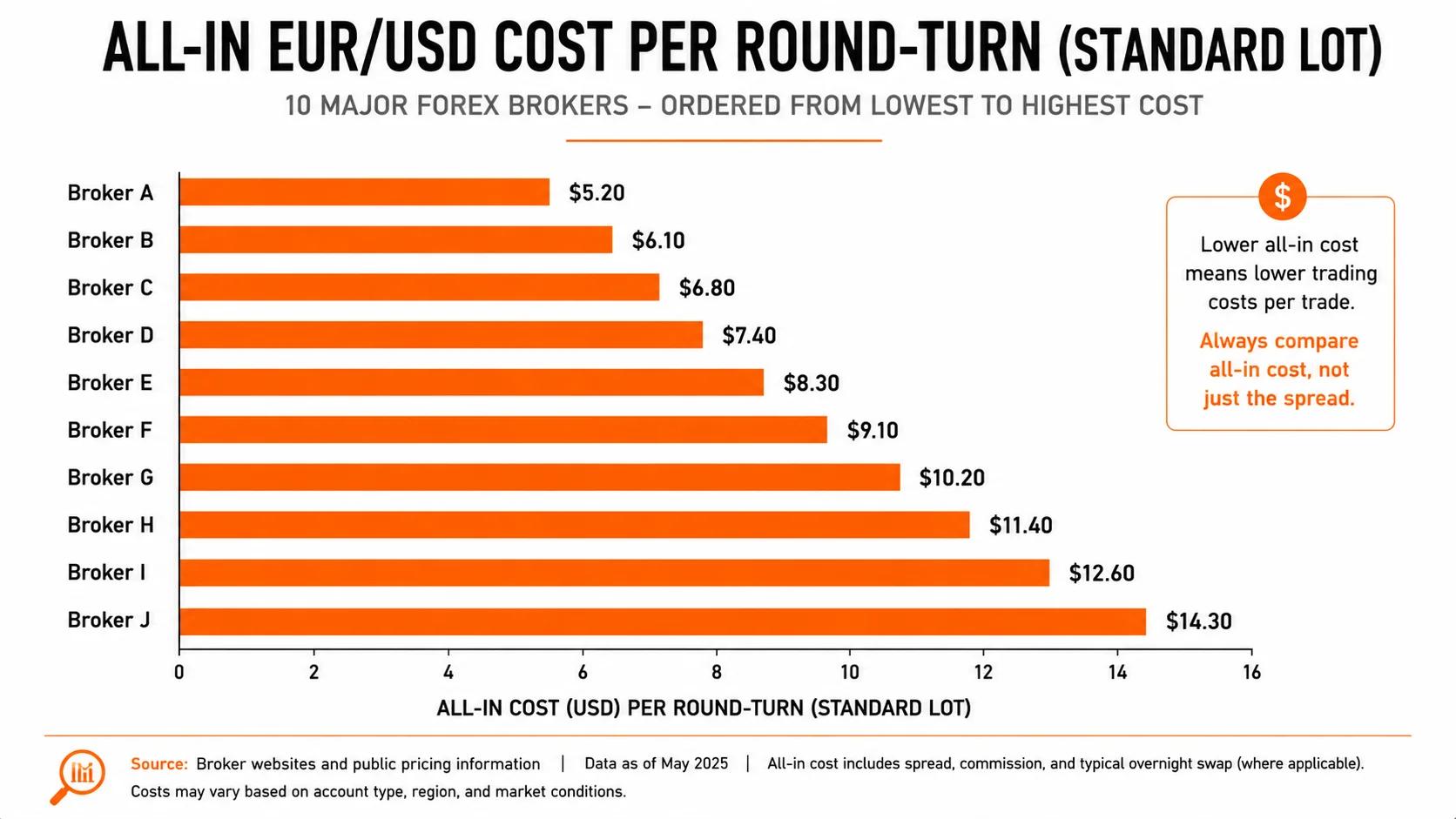

The Real Cost Model: Beyond the Spread

Spread + Slippage + Commission = True Cost Per Trade

The true cost of a trade is the spread, plus any per-lot commission, plus the slippage you experience on entry and exit.

Using illustrative figures: if you trade EUR/USD with a 0.1 pip spread and 0.1 pip average slippage on both entry and exit, your real per-trade cost is 0.3 pips before commission. A competitor offering a 0.3 pip spread with zero slippage matches you on real cost, even though their headline number looks worse.

The formula:

True Cost = Spread + Commission (in pip equivalent) + Average Slippage

Run that across 100 trades and the differences compound quickly. The broker that looked cheaper on paper often is not.

How Execution Quality Changes the Math for Different Trading Styles

The weight you give execution quality depends on how tight your per-trade margin is.

- Swing traders holding positions for days will find a few tenths of a pip in slippage per trade largely immaterial against a multi-hundred pip target. Execution quality matters, but it is not the dominant variable.

- Scalpers targeting 3 to 5 pips per trade face a different calculation. Even 0.5 pips of average slippage represents 10 to 17% of the target profit, before spread.

- High-frequency traders running automated strategies with tight logic can find execution quality determining whether a strategy is profitable at all.

The tighter your per-trade margin, the more execution quality matters.

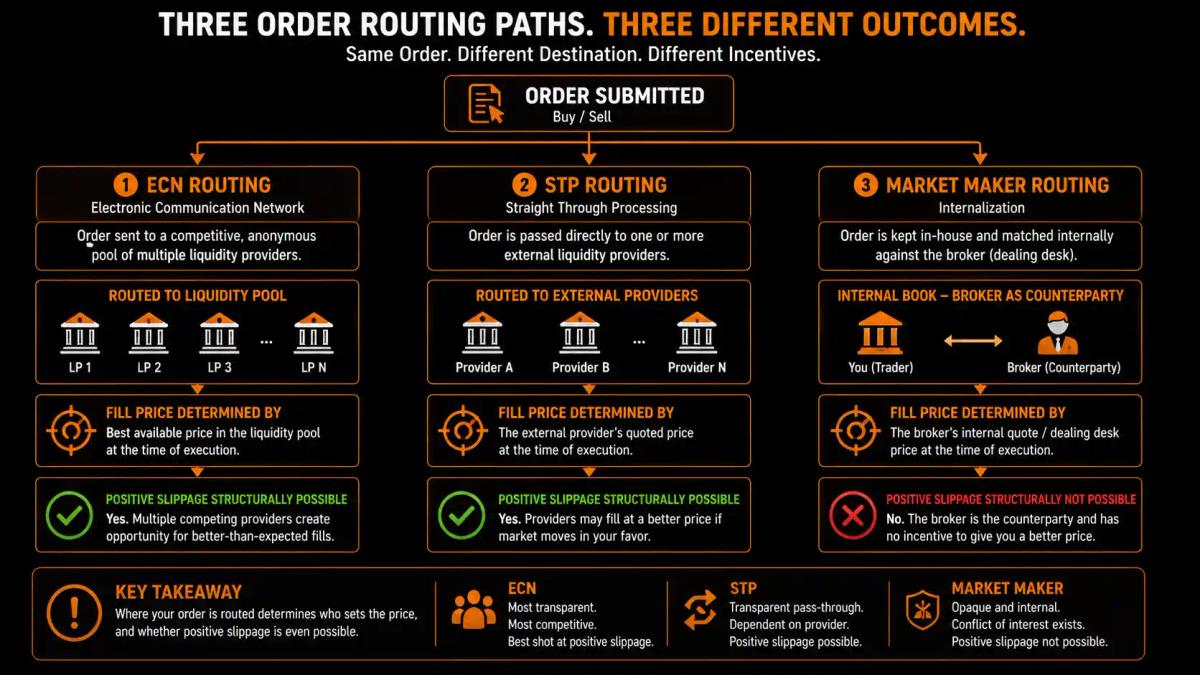

How Smart Liquidity Routing Affects Your Fills

What Liquidity Routing Is and Why It Matters

When you submit an order, it has to go somewhere to be filled. Liquidity routing is the process that determines where: which liquidity provider, at what price, through which pathway.

Smart liquidity routing means your broker's system is actively seeking the best available fill across multiple providers. Poor routing means your order goes to whoever the broker has a standing arrangement with, regardless of whether that is the best price at that moment.

ECN, STP, and Market Maker: How Routing Model Affects Execution

These three models describe how your broker handles your order.

ECN (Electronic Communication Network): Orders are matched directly with other participants, including banks, institutions, and other traders, in an anonymous pool. Spreads are variable and reflect real market liquidity. You pay a commission. Price improvement through positive slippage is possible.

STP (Straight-Through Processing): Orders are routed directly to one or more external liquidity providers without a dealing desk. There is no manual intervention, but unlike ECN, you may be routed to a single provider rather than a competitive pool. Execution is generally cleaner than market maker, though the outcome depends heavily on the quality of the broker's liquidity relationships.

Market Maker: The broker takes the other side of your trade internally, creating a market for you. This gives them more control over pricing and execution, which is a structural difference, not an automatic problem. Some market makers offer very consistent execution under normal conditions, with prices derived from underlying liquidity. The risk is that their execution incentives can diverge from yours during volatile periods.

How to Evaluate a Broker's Execution Quality Before You Commit

Best execution standards exist in regulated markets. Where rolling spot forex or CFDs are the instrument in question, MiFID II Article 27(1) requires brokers authorised in Europe to take all sufficient steps to obtain the best possible result for clients.

Spot forex contracts fall outside MiFID II's best execution obligations. Regulation sets a floor, not a ceiling. Within compliant execution, there is still enormous variation.

What to Ask and Where to Look

When researching a broker's execution quality, look for:

Execution statistics: Average fill speed, slippage distribution, reject rate. Some brokers publish these; many do not. Their absence is itself informative.

Order execution policy: Every regulated broker should publish one. Look for specifics on how they handle slippage, their latency targets, and which liquidity providers they use. Vague policies with no measurable commitments are a flag.

Infrastructure disclosure: Where are their servers? Brokers that do not mention infrastructure at all rarely have much to be proud of.

Third-party verification: Some brokers provide independently verified execution statistics. That is worth considerably more than broker-written copy.

Red Flags in Broker Execution Disclosures

Watch for these:

- Spreads advertised as "from" a low figure. That number applies to a small fraction of trading hours.

- No slippage disclosure or policy. A broker unwilling to discuss slippage in writing is telling you something.

- Order execution policies that describe process but commit to no measurable standard. Process without accountability is not a policy.

- Positive slippage not mentioned. Brokers that only discuss slippage in one direction are telling you something about how they handle the other.

- Commission rates that seem unusually low on ECN or STP accounts. Prime-of-prime liquidity access has a cost; if the economics do not add up, something else does.

Testing Execution Quality with a Live Account

The only reliable test is live trading with real money. Demo accounts do not replicate live execution. You can do this with a minimum deposit. Trade across a variety of conditions:

- Trade during multiple sessions: London open, New York overlap, and quieter Asian hours.

- Trade around one or two scheduled economic releases, avoiding the very largest ones.

- Record your requested price and filled price for every trade.

- Calculate your average slippage on entries and exits separately.

- Note any requotes or rejections.

Ten to twenty trades across different conditions gives you enough data to see whether the broker's execution is consistent with their marketing. If slippage runs consistently negative and never positive, you have your answer.

Which Trader Types Are Most Exposed to Execution Risk

Scalpers and High-Frequency Traders

Scalpers are the most execution-sensitive traders in the market. When your profit target is 3 to 5 pips, a 0.5 pip average slippage on entry and exit is taking a meaningful share of every trade. Latency matters enormously here. Any delay between signal and fill in a fast-moving market changes the trade. Requotes are particularly damaging because they typically arrive after the opportunity has already passed.

For scalpers, execution quality is the primary consideration, not a secondary one.

News Traders

Traders who target high-impact economic releases face the most extreme execution conditions in retail forex. Liquidity evaporates in the seconds before and after a major release, spreads widen sharply, and fill quality degrades even on quality infrastructure.

Some brokers restrict trading around news events entirely, a policy that protects their risk exposure while limiting yours. Others widen spreads to levels that make the trade unviable regardless of the outcome. If news trading is part of your strategy, understanding a broker's specific policy on it is not optional.

Swing and Position Traders

Execution quality matters less at longer timeframes, but it does not disappear. A swing trader entering on a daily close does not feel 50ms latency. Consistent negative slippage still accumulates across a year of trading, and wide spreads during entry windows still affect total cost.

For swing and position traders, the more relevant execution factor is price stability: whether the broker holds tight prices consistently at your typical entry times, or widens spreads during the periods when you are most likely to be active.

How MonkeyTrade Tests Broker Execution

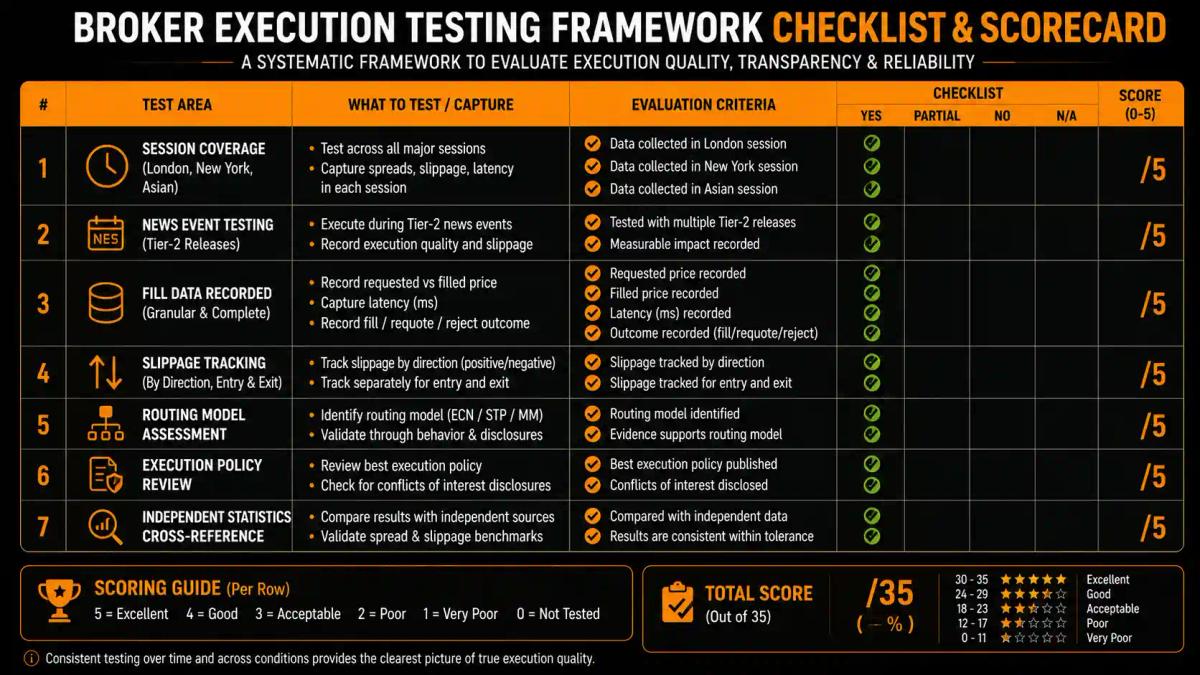

Broker marketing describes conditions. Live testing reveals them. MonkeyTrade evaluates execution quality through a structured programme of real-money trading across a standardised set of conditions, designed to surface the gaps that advertised specifications never show.

Testing runs across multiple sessions, covering the London open, the New York overlap, and the quieter Asian hours, to capture how execution holds up across different liquidity environments. Each test includes trading around scheduled economic releases at the tier-2 level, where liquidity thins enough to stress execution without triggering the extreme conditions that make any fill unreliable.

For every trade placed, MonkeyTrade records:

- The requested price and the filled price

- The time elapsed between order submission and confirmation

- Whether the order was filled, requoted, or rejected

Slippage is calculated separately for entries and exits, and tracked across both directions. A broker that passes positive slippage consistently is treated differently from one where slippage only ever moves against the client.

The routing model is assessed alongside the live results. Order execution policies are reviewed for measurable commitments rather than process descriptions, and infrastructure disclosure is cross-referenced against fill quality during high-latency periods. Where brokers publish independent execution statistics, those figures are compared against observed results.

The output is a composite execution score weighted by trading style relevance. Brokers are assessed separately across:

- Scalping-relevant conditions, where latency and slippage frequency matter most

- Swing-relevant conditions, where price stability at entry is the primary variable

A broker that performs well across both profiles earns a different rating from one that performs well in only one.

No demo account data is used. All results are drawn from live trading with real capital at risk.

What Best Execution Actually Looks Like in Practice

The best execution experience is mostly invisible. Prices fill where you expect, slippage is small and runs in both directions, requotes are rare, and your actual trading costs match what the broker's model predicts. You are not spending time wondering whether the infrastructure is working against you.

Reaching that standard requires active evaluation, and far fewer traders do it than should. Evaluating a broker means looking past the spread column and assessing execution quality directly:

- Check infrastructure disclosure

- Read order execution policies for specifics rather than generalities

- Test fills with real money across different sessions

- Apply the true cost model rather than relying on advertised spread figures alone

Every low-spread headline sits in front of a total cost calculation. Run it.

Frequently Asked Questions

What is the difference between spread and execution quality?

The spread is the difference between the buy and sell price quoted by your broker. It is one component of your trading cost. Execution quality is a broader measure that includes how closely your actual fill matches that quoted price, how quickly the order is processed, how often you receive the price you requested, and how stable pricing is across different market conditions. A tight spread with poor execution can cost more than a wider spread with clean fills.

How do I test a broker's execution quality before depositing a large amount?

Open an account with the minimum deposit and trade it across different sessions and market conditions, ideally including at least one scheduled news release. Record your requested price and your filled price for every trade, and track any requotes or rejections. Calculating your average slippage over 15 to 20 trades gives you real data on execution consistency. Demo accounts do not replicate live execution, so this small live test is the only reliable method.

Does execution quality matter more for some trading styles than others?

Yes. Scalpers and high-frequency traders are most exposed, because slippage and latency represent a large proportion of their per-trade profit target. News traders face extreme execution conditions around high-impact releases. Swing and position traders are less affected by latency but still benefit from consistent pricing and low average slippage across their trade entries and exits.

What is slippage, and does positive slippage actually happen?

Slippage is the difference between the price you requested and the price you received. Negative slippage means you got a worse price: you bought higher or sold lower than intended. Positive slippage means you got a better price than requested. Both are real, and both happen in live trading. A broker with genuinely good execution passes positive slippage to clients. If slippage only ever runs in one direction, that pattern is worth paying close attention to.

How do I interpret execution statistics if a broker publishes them?

Look at average fill speed (lower is better), the percentage of orders filled at the requested price, and, where available, slippage distribution showing both positive and negative outcomes. Reject rates and requote rates are also useful. Be sceptical of statistics that only show best-case figures or that do not specify the market conditions under which they were measured. Independent third-party verification carries more weight than figures produced by the broker.

About the authors

Related articles

The True Cost of Trading: A Data-Driven Comparison Across 10 Forex Brokers

Full-cost comparison across spreads, commissions, swap rates, and fees for 10 major forex brokers; including EUR/USD, GBP/USD, and Gold trading costs per lot.

7 Moments to Be Bullish on Gold (When to Buy Gold and Why It Matters)

Discover 7 key moments that signal when to buy gold, from real rate shifts to dollar weakness and central bank demand.

Best Day Trading Platforms: Features, Fees, and Execution Speed Compared

A structured comparison of the best day trading platforms: execution latency, spreads, FCA leverage caps, tax reporting, and the psychological tooling that separates disciplined traders from

0 comments