The Prop Firm Industry Is Overdue for a Shakeout - Here's What Comes Next

The prop firm industry is under serious structural pressure.

Firms are closing, payouts are being delayed or disputed, and regulatory bodies are asking harder questions. This article breaks down how the funded trader model actually makes money, why cracks are forming, and what a more mature, post-shakeout industry looks like for traders who want to navigate it intelligently.

The Funded Trader Model: How It Actually Makes Money

Most traders assume prop firms make money the way a hedge fund does: by deploying capital and capturing returns. That assumption is worth examining closely, because the economics of most prop firms work quite differently.

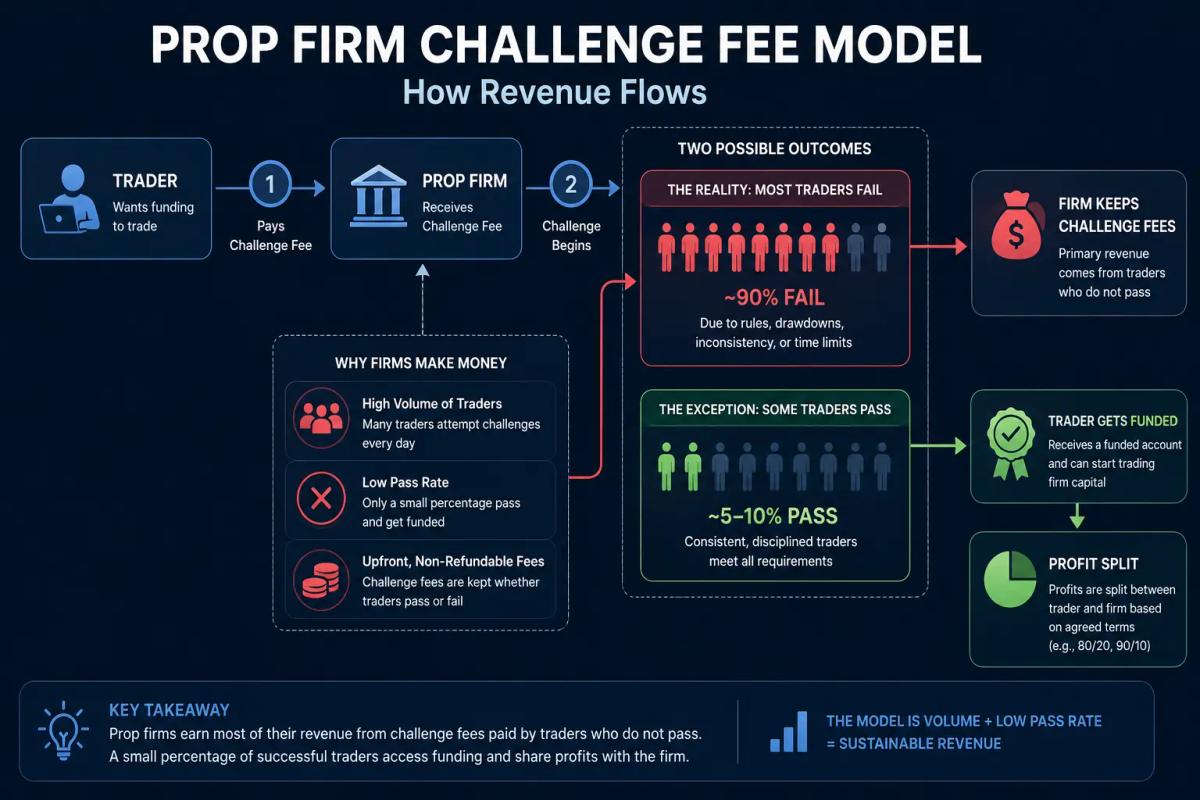

Challenge Fees as the Primary Revenue Engine

The core product most prop firms sell is access to an evaluation. You pay a fee, attempt to hit profit targets within drawdown limits, and if you pass, you gain access to a funded account. The firm takes a cut of any profits you generate on that account.

This sounds like a trading partnership. But in practice, for a large share of firms, the challenge fee is the business model. Consider the math:

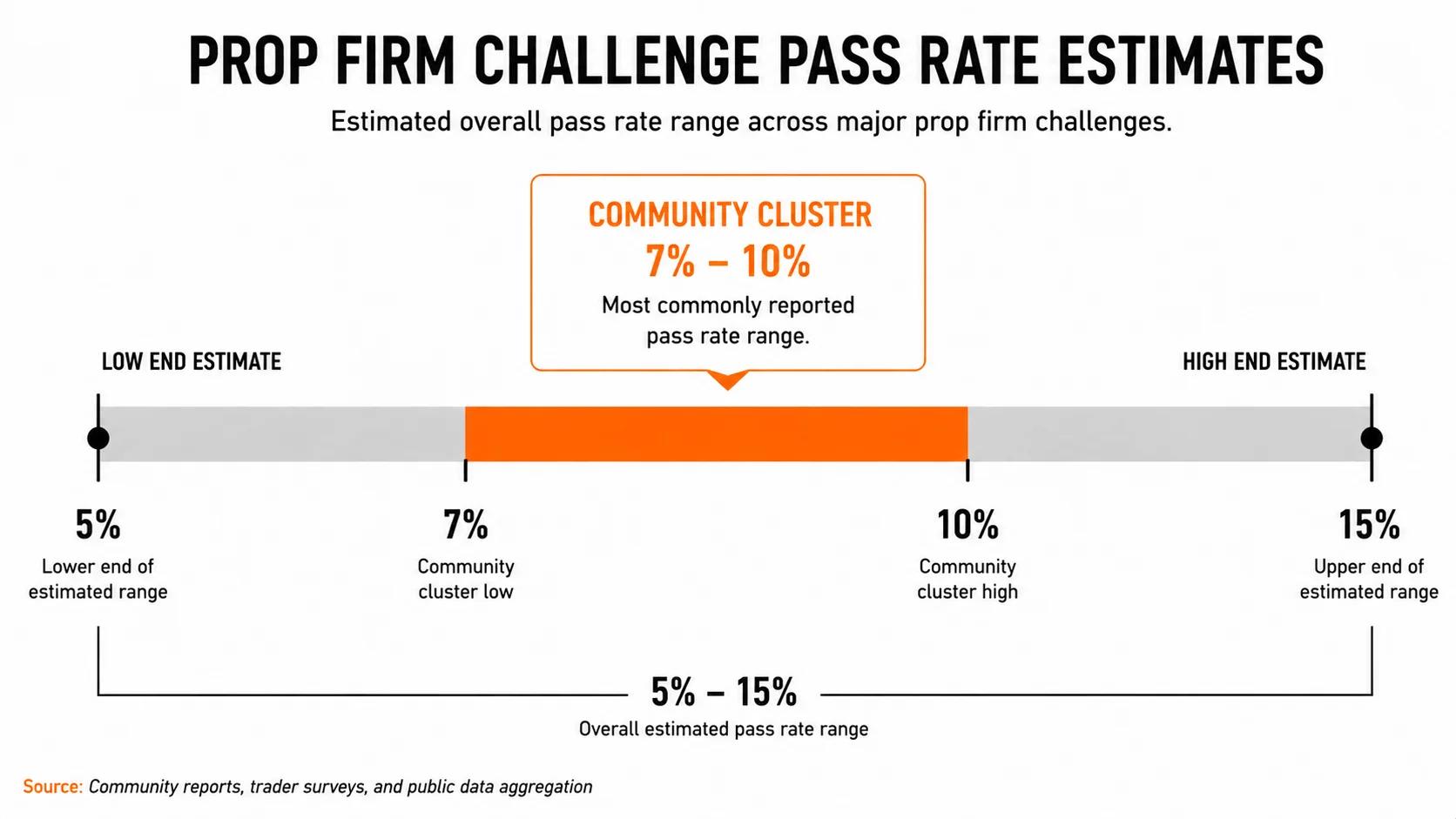

- The majority of traders fail challenges. Industry estimates commonly suggest 80-90% fail rates, though firms do not publish verified data.

- A failed challenge means the firm keeps the fee with no payout obligation.

- Even traders who pass often reset, retry, or upgrade to larger accounts, generating more fee revenue.

- Actual payouts to consistently profitable traders represent a relatively small portion of total revenue for many operators.

Challenge fees are a predictable, high-volume revenue stream. Trading profits from funded accounts are not.

Why Most Prop Firms Are Not Trading Firms

A genuine proprietary trading firm allocates real capital to traders and profits when those traders are profitable. Most retail prop firms do not operate this way. When you trade a funded account at most retail prop firms, you are typically trading in a simulated environment or under counterparty arrangements that insulate the firm from your actual trade results.

The firm's financial health is tied to challenge fee volume, payout obligations, and operational costs. That is the economic structure you are dealing with, and it is the lens through which you should evaluate any firm's sustainability.

The Pressure Points Building Across the Industry

The challenge fee model works smoothly when new trader sign-ups consistently exceed payouts owed to successful traders. When that balance tips, the pressure becomes visible fast.

Regulatory Scrutiny Is Increasing

Regulators have started paying closer attention to the prop firm space. The key question many are asking is whether prop firm challenge products constitute financial instruments or investment products that require licensing.

In the UK, the FCA has publicly indicated awareness of the prop firm sector and its potential overlap with regulated activities.

In the US, the CFTC and NFA have historically focused on forex broker regulation, but firms with US client bases are facing increasing scrutiny over whether their structures constitute off-exchange derivatives trading.

The direction is clear, though: firms built on regulatory arbitrage, operating in jurisdictions with lighter oversight or on business models that sidestep licensing requirements, face real exposure as that arbitrage window narrows.

The Payout Problem: When Volume Outpaces Capital

Payout complaints are the earliest visible sign of a firm under financial strain. When a firm's inflow of challenge fees slows while its base of successful funded traders continues to grow, the mismatch hits the payout queue first.

In practice, this tends to look like:

- Payout processing times lengthening from days to weeks.

- New terms or conditions retroactively applied to funded accounts.

- Disputes over rule violations that traders feel were not clearly communicated.

- Withdrawal limits being quietly reduced or restructured.

These are not always signs of outright fraud. Sometimes they reflect poor financial planning, rapid growth without adequate capital reserves, or operational inexperience. The outcome for the trader is the same either way.

Market Saturation and the Race to the Bottom on Fees

The number of retail prop firms grew dramatically between 2020 and 2024. Low barriers to entry, including white-label trading platforms, turnkey challenge infrastructure, and aggressive affiliate marketing, made it possible to launch a prop firm with relatively modest startup capital.

The result is hundreds of firms competing for the same trader pool, differentiated largely on price. Challenge fees dropped, account sizes increased, and profit splits grew more generous. A business model that depends on thin margins and growing payout obligations has limited room for error.

A race to the bottom on fees only ends one way for the weakest operators.

What Recent Firm Closures Tell Us

Firm closures in this space have not been random. They follow recognisable patterns, and understanding those patterns gives you useful signal for evaluating firms you might engage with.

Common Failure Patterns

Looking at firms that have shut down or faced serious disruption, a few structural vulnerabilities appear repeatedly.

Regulatory action as a trigger: MyForexFunds (MFF) provides a complicated illustration of how regulatory intervention can disrupt a large prop firm, and of the limits of that intervention. The firm was shut down in 2023 following action by the CFTC and the Ontario Securities Commission. The subsequent legal proceedings did not go as the regulators intended: the CFTC's case was dismissed with prejudice, with a federal judge sanctioning the CFTC for acting in bad faith, and the Ontario court awarded costs against the OSC. MFF has since announced it will honour pre-shutdown payout requests. The case does not support a simple cautionary narrative, but it does demonstrate that regulatory action alone, even when ultimately unsuccessful, can suspend a firm's operations for an extended period and leave traders in limbo for years. Operational continuity risk is real, regardless of how legal proceedings eventually resolve.

Payout disruption preceding collapse: In multiple cases, traders reported escalating payout issues months before a firm officially ceased operations. The payout queue is often the canary.

Opacity about financial structure: Firms that cannot clearly explain how they manage funded account risk, where their capital comes from, or how payouts are funded tend to be the ones that struggle when challenged.

Aggressive affiliate dependency: Firms that rely heavily on affiliate marketing for new trader acquisition are particularly exposed when sign-up volume drops. A funded trader model that depends on constant new challenge purchases to cover payouts is structurally fragile.

What Traders Were Left With

When a firm closes or suspends operations, the near-term outcomes for traders are generally poor, even if longer-term resolution eventually follows. Challenge fees paid are not recoverable through standard consumer protection routes in most jurisdictions. Funded account balances are not real capital deposits, and formal recourse mechanisms are limited for traders dealing with unregulated operators.

Traders caught in operational suspensions have often faced extended periods without access to pending payouts, with uncertain timelines and limited visibility into proceedings they have no standing in. That exposure, regardless of how a firm's legal situation ultimately resolves, is worth factoring into your decisions before you engage.

What a Post-Shakeout Industry Looks Like

Industries reorganize around structural pressure. The prop firm space is not heading toward extinction; it is heading toward a sorting event that separates durable models from brittle ones.

Regulatory Compliance as a Competitive Advantage

Firms that are proactively engaging with regulators, restructuring products to meet financial services requirements, and operating with genuine transparency about their model will be better positioned as regulatory pressure increases.

This is already happening. Some firms are restructuring as regulated entities, obtaining licences in relevant jurisdictions, and marketing compliance as a differentiator. For traders, this matters practically: a regulated firm operating under financial services law carries different accountability obligations than an unregulated operator.

Regulation in this context functions as a forcing function. It penalises corner-cutting and rewards operators who built sustainably.

Consolidation: Fewer Firms, Stronger Models

Expect the number of active retail prop firms to contract. The math of the current market, with too many competitors, compressed margins, and growing payout obligations, points toward consolidation. Larger, better-capitalised firms will absorb market share as smaller operators fail or exit.

FTMO, TopStep, and The5ers have demonstrated that it is possible to build durable operations with real infrastructure and genuine trader communities. These firms have shown staying power that newer, thinner operations have not.

The firms that survive this consolidation will likely share a few characteristics:

- Transparent, documented financial structures.

- Established track records on payouts.

- Regulatory compliance or active engagement with licensing requirements.

- Diversified revenue beyond challenge fee volume alone.

The Shift Toward Hybrid and Compliant Structures

Some firms are moving toward hybrid models that incorporate regulated brokerage elements alongside prop trading structures. Others are exploring arrangements where successful traders transition to trading real capital under formal terms.

These models are more operationally complex and more expensive to run. That is precisely why they tend to attract more serious operators and produce more stable outcomes for traders.

How to Protect Yourself as a Funded Trader

No amount of due diligence eliminates risk entirely in an unregulated space. Informed decision-making does meaningfully reduce your exposure.

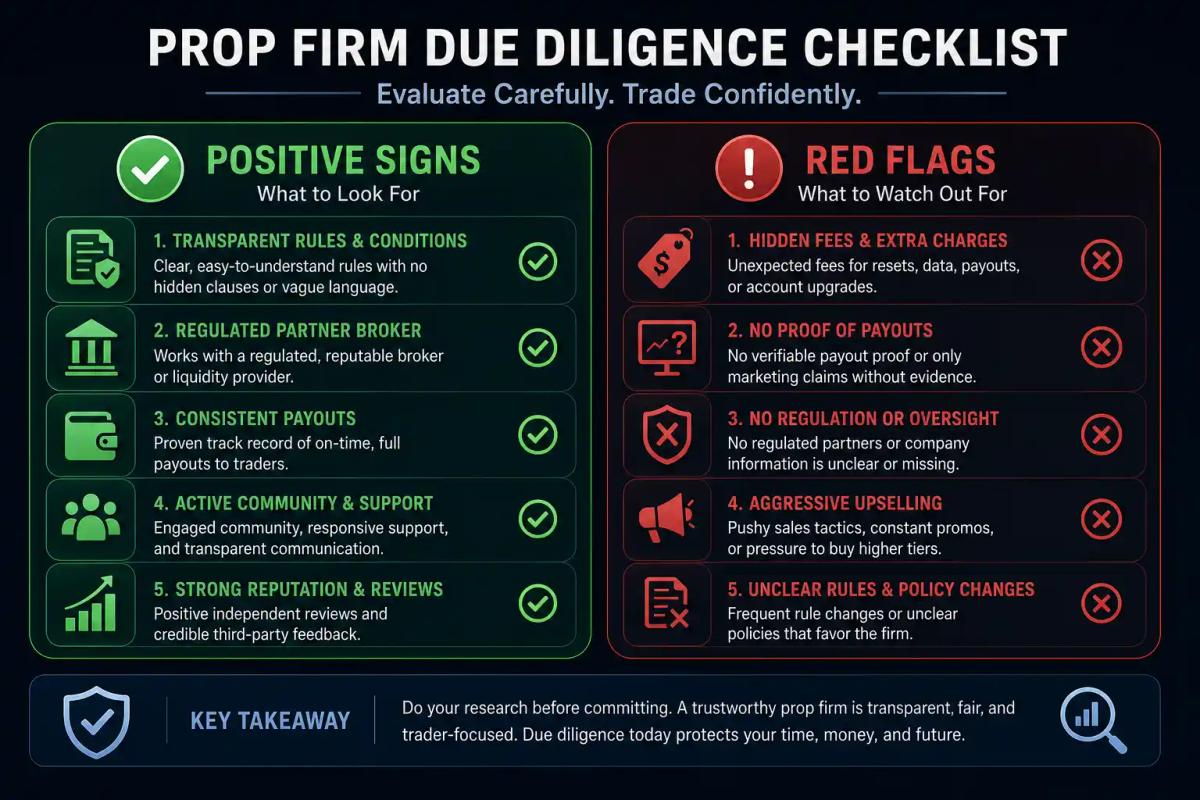

Red Flags to Watch Before You Buy a Challenge

When comparing prop firms, and before paying any challenge fee, look for these warning signs:

- Payout complaints are widespread and recent: Check trader communities (Reddit, Discord, trading forums) for current payout experiences, not just testimonials on the firm's own site.

- No clear information on financial structure: If the firm cannot explain how it manages funded account risk, that gap is worth noting.

- Terms and conditions that are vague or frequently updated: Retroactive rule changes are a common precursor to payout disputes.

- Heavy affiliate marketing with thin trader community substance: A firm that is primarily a marketing operation with shallow trader support infrastructure carries a different risk profile than one with genuine community depth.

- No verifiable history: Firms launched within the last 12-18 months have not been stress-tested through a difficult market environment.

- Regulatory status is unclear or actively avoided in communications: Legitimate operators can state clearly where and how they operate.

What Due Diligence Actually Looks Like in 2025-2026

Practical due diligence on a prop firm now includes the following steps.

Check regulatory status directly. Search the FCA register, CFTC databases, or relevant jurisdiction registries. Operating without regulation is a data point, not automatically disqualifying, but it changes your risk profile.

Verify payout track record independently. Look for verified payout screenshots and community discussion outside of firm-controlled channels. Recent data matters more than historical reputation.

Read the full terms before paying. Pay specific attention to: drawdown calculation method, payout processing timelines, acceptable trading behaviours, and what happens to your funded account if the firm changes its terms.

Size your challenge fee spend as a risk position. Treat challenge fees the way you would treat a speculative trade. Only commit what you can absorb losing entirely. Spreading two smaller challenges across different firms is lower-risk than a single large challenge at one firm.

Monitor firm communications after joining. Changes in payout processing times, customer support quality, or communication tone are operational signals. Pay attention to them.

Conclusion: The Industry Is Not Dying - It Is Being Tested

The prop firm industry grew fast, attracted operators of wildly varying quality, and is now experiencing the consequences of that rapid, under-regulated expansion. That is a normal, if painful, part of how industries mature.

The underlying value proposition, giving skilled traders access to capital they would not otherwise have, is real and unlikely to disappear. What is disappearing is the ability to operate carelessly in a regulatory grey zone with no financial reserves and call it a prop trading firm.

As a trader, this moment requires clarity about what you are actually participating in. You are buying access to an evaluation product from a company whose economics are driven primarily by fee volume. That can still make sense, under the right conditions, with the right firms. The prop firm industry's future will be smaller, more regulated, and more honest about what it is. That is not a bad outcome; it is a more stable one.

The traders who come out ahead are not the ones who abandon the space. They are the ones who understand it clearly enough to choose well within it.

Frequently Asked Questions

Is the prop firm model legal, and how does it differ from a regulated broker?

Retail prop firms generally operate in a legal grey area rather than being explicitly illegal, but their legal status depends heavily on jurisdiction and how their products are structured. Unlike regulated brokers, most prop firms are not licensed financial services entities, which means you do not have the same protections, including compensation schemes, dispute resolution mechanisms, and capital adequacy requirements, that apply to regulated firms. The legality of specific structures is being actively evaluated by regulators in several jurisdictions.

What happened to MyForexFunds, and what should traders take from it?

MyForexFunds was shut down in 2023 following action by the CFTC and the Ontario Securities Commission. The legal proceedings that followed were protracted and did not ultimately favour the regulators: the CFTC's case was dismissed with prejudice, with a federal judge sanctioning the CFTC for bad faith conduct, and the Ontario court awarded costs against the OSC. MFF has since announced it intends to honour pre-shutdown payout requests. The case does not offer a straightforward lesson about regulatory enforcement producing trader protection. If anything, it illustrates that regulatory action can suspend a firm's operations and freeze trader funds for extended periods, regardless of how proceedings eventually resolve. The practical takeaway is about operational risk: even a firm not ultimately found to have acted wrongly can leave traders in limbo for years while legal processes run their course.

How can I tell if a prop firm is financially stable before paying for a challenge?

There is no publicly available financial reporting requirement for most unregulated prop firms, so direct financial verification is not possible. What you can assess indirectly: payout track record through independent community sources, operational history length, transparency about financial and risk management structure, and current regulatory status. Firms with consistent, verified payout histories over multiple years across varied market conditions have at least demonstrated operational durability.

Will regulation kill the prop firm industry or improve it?

Evidence from adjacent industries suggests regulation tends to professionalise rather than eliminate. Firms that cannot meet basic licensing and capital requirements will exit, and some of those will be the riskiest operators. Firms that adapt to regulatory requirements will operate with more accountability and, likely, more genuine capital reserves. The industry may shrink in terms of firm count, but the firms that remain are more likely to be sustainable operations.

What is the difference between a sustainable prop firm model and a challenge-fee-dependent one?

A sustainable model generates revenue from multiple sources, including genuine profit participation from consistently profitable traders, and maintains adequate reserves to cover payout obligations even when new challenge sign-ups slow down. A purely challenge-fee-dependent model requires constant new trader acquisition to remain solvent. Any significant slowdown in new sign-ups creates immediate payout pressure. That structural fragility is the distinction that matters.

Does passing a prop firm challenge still make financial sense in 2025-2026?

It depends entirely on which firm you are dealing with and how you approach the cost. For firms with verified payout histories and transparent operations, passing a challenge can provide meaningful leverage on your trading capital; that core value proposition has not changed. The risk is firm-level: you may pass legitimately and still not receive payouts if the firm is in financial difficulty. Sizing your challenge spend as a risk position you can afford to lose entirely, and concentrating on well-established firms, is the rational approach.

What should I do if my prop firm closes or stops paying?

Your practical options are limited in an unregulated context. Document everything immediately: screenshots of your account status, payout requests, communications, and terms at the time you signed up. Check whether the firm has any regulatory status in your jurisdiction that might provide a complaints mechanism. If the firm is based in a jurisdiction with small claims or consumer protection routes, assess whether the amounts involved make that viable. For most traders, the realistic outcome is absorbing the loss and redirecting to a more stable firm.

About the authors

Related articles

The Real Pass Rate of Prop Firm Challenges: What the Data Shows

Most prop firm challenges have low pass rates - but what does the data actually show? We break down the numbers, the reasons, and what they mean for you.

How Long Does It Take to Get Funded by a Prop Firm?

Realistic timeline breakdown from signup to funded status across FTMO, The5ers, TopStep, FundedNext, and E8 — including challenge phases, minimum trading days, and processing times.

I Passed 3 Prop Firm Challenges Before I Failed One: Here's What I Learned

Passing three prop firm challenges didn't prepare me for failing the fourth. Here's what changed, what broke down, and what I'd do differently now.

0 comments