Is European Overregulation Killing the Region’s Stock Market?

European stock market regulation is one of the most consequential and most misunderstood forces shaping how retail traders access EU markets today. This piece breaks down exactly which rules are creating friction, how they compare to conditions in the US, and what your practical options are if you’re operating inside the EU regulatory framework.

The Case for the Prosecution: Where EU Regulation Creates Real Friction

EU regulation shapes what you can trade, how much leverage you can use, and which brokers are willing to serve you at all. Some of those constraints are deliberate, others are side effects. All of them affect your account.

ESMA Leverage Restrictions and What They Actually Limit

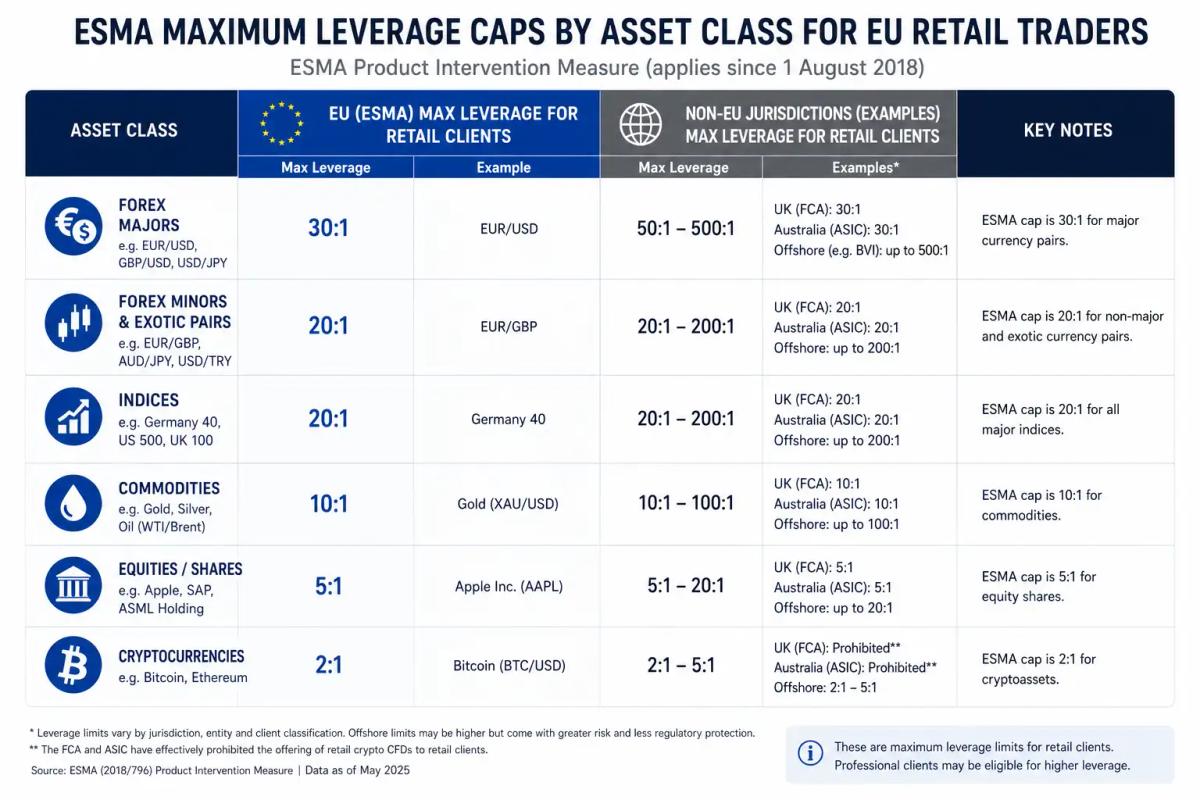

ESMA, the European Securities and Markets Authority, introduced product intervention measures in 2018 that cap the leverage available to retail clients across all major CFD and derivative categories. These are hard ceilings, and they apply to every broker regulated in the EU.

Here’s what those caps look like in practice:

Consider what this means in concrete terms:

With a EUR 10,000 account, the 30:1 cap on a forex major pair gives you EUR 300,000 in notional exposure. At 500:1, the limit available to retail clients through many offshore brokers, that same account controls EUR 5,000,000. That restructures your entire position sizing logic.

For many retail traders, particularly those running strategies that depend on capturing small moves in liquid instruments, the ESMA caps make certain strategies economically unworkable at smaller account sizes.

MiFID II Compliance Costs and the Broker Exodus Effect

MiFID II, the Markets in Financial Instruments Directive II, came into force in January 2018 and represents one of the most comprehensive regulatory overhauls in European financial market history. On paper, it’s a framework for improving market transparency, investor protection, and best execution. In practice, it’s also an exceptionally expensive framework to operate inside.

The compliance burden MiFID II imposes on brokers includes:

- Transaction reporting: Every trade must be reported to regulators in near-real-time, with detailed counterparty and instrument data.

- Best execution obligations: Brokers must demonstrate they’re consistently achieving the best available outcome for clients across price, speed, and likelihood of execution.

- Product governance: Financial products must be designed, tested, and continuously reviewed for their target market.

- Research unbundling: Investment research must be paid for separately from execution, ending decades of bundled commission arrangements.

- Client classification and suitability assessments: Significant documentation requirements for onboarding and ongoing client management.

For large institutional operators, these costs are absorbed across enormous revenue bases. For smaller or mid-size retail brokers, they represent a structural margin compression that many simply cannot sustain.

The result is a measurable contraction in the number of brokers actively competing for EU retail business. Several relocated operations to the UK (post-Brexit), Cyprus, or entirely outside EU jurisdiction following MiFID II implementation. Others withdrew certain products or markets from EU retail access altogether. If the EU broker market feels thinner than it did a decade ago, that’s because it is.

Retail Investor Access: What EU Traders Cannot Trade

Leverage caps and compliance costs are the headline story, but EU regulation also restricts what retail clients can access directly.

As a retail client under EU regulation, you may find yourself locked out of:

- Binary options: Banned outright for retail clients across the EU by ESMA in 2018.

- Certain complex CFDs: Subject to mandatory risk warnings, leverage caps, and in some cases restricted availability depending on national regulator implementation.

- Some structured products: Subject to the EU’s Packaged Retail and Insurance-based Investment Products (PRIIPs) regulation, which creates disclosure requirements that some non-EU product issuers choose not to meet, making those products inaccessible to EU retail clients.

- US-listed ETFs: A notable consequence of PRIIPs rules means that most US-domiciled ETFs, including popular index funds tracking the S&P 500, cannot be marketed or sold to EU retail investors, because they don’t produce the required Key Information Document (KID) in the required format.

That last point deserves emphasis. If you’re an EU retail investor who wants direct exposure to the S&P 500 via a US-listed ETF, a straightforward, low-cost strategy that’s standard for American investors, your broker almost certainly cannot offer it to you. You’d need to use a European-domiciled equivalent, which may carry different costs, liquidity profiles, or currency exposures. It’s a meaningful restriction on your investment toolkit, even if it’s not an insurmountable one.

Does the US handle this better? Not across every dimension, but the structural comparison is worth examining directly.

EU vs. US: A Structural Comparison

The gap between European and American capital markets isn’t purely a regulatory story, but regulation is a significant part of it. Understanding the structural differences helps you assess whether the friction you’re experiencing is unique to EU rules or simply a feature of less developed retail market infrastructure.

Market Depth, Liquidity, and Retail Participation Rates

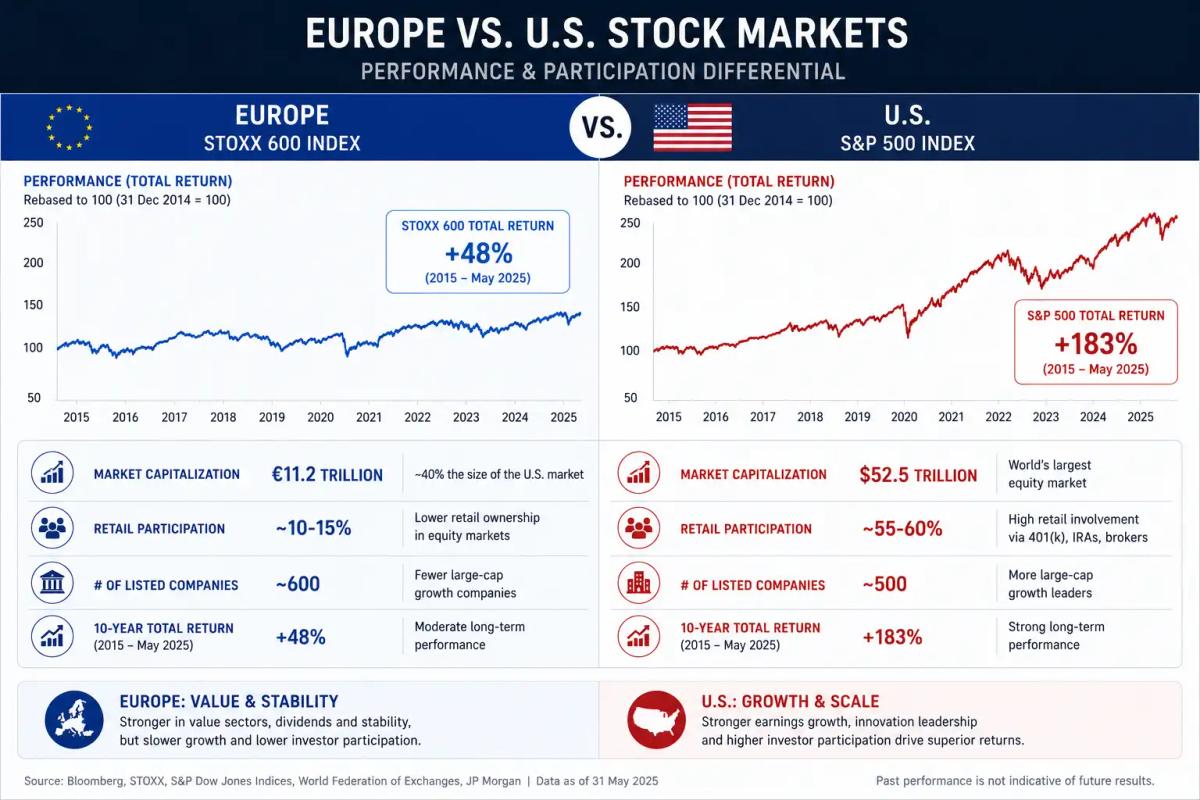

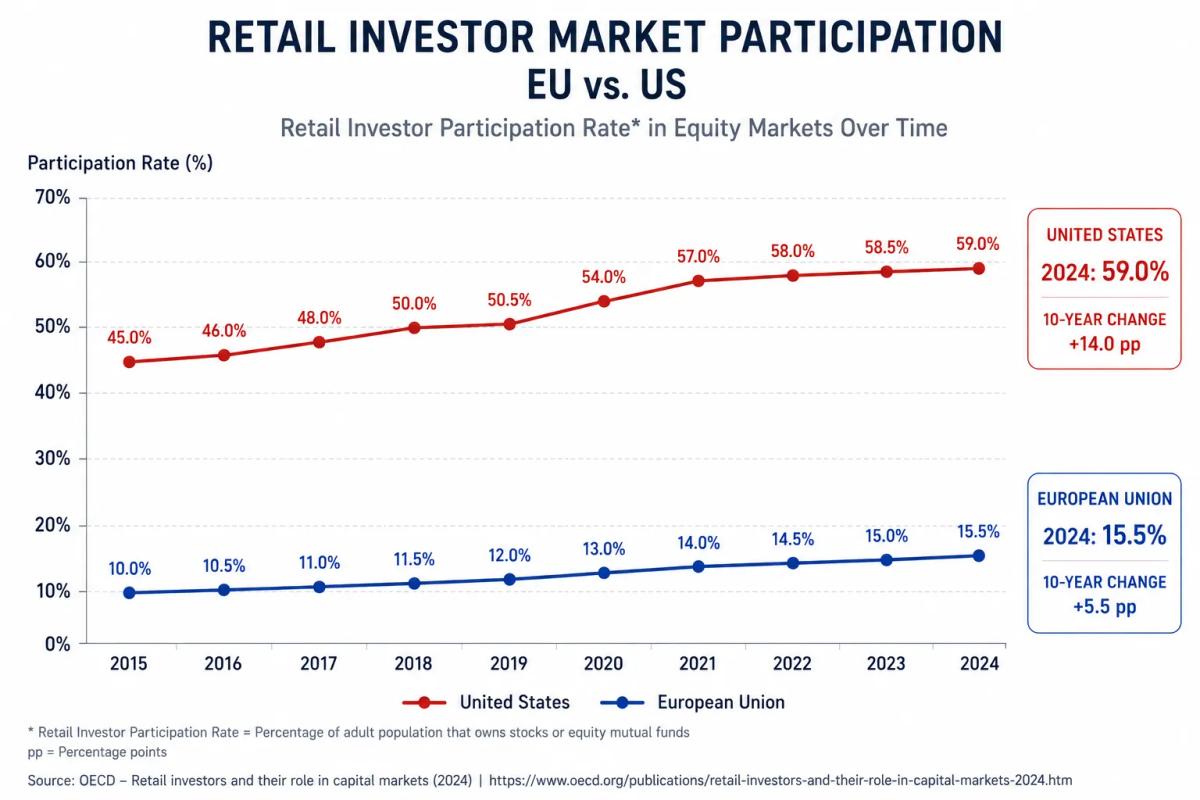

The US stock market dwarfs European equivalents by almost every measure. The S&P 500 alone carries a market capitalisation that exceeds the combined value of most major European indices. More relevant for retail traders is the difference in retail participation.

US retail participation in equity markets is roughly in the 55% to 60% range of households, depending on the source and measure used, while Gallup reported 61% of U.S. adults owning stock in 2023 and 62% in 2025. EU household equity ownership, whether measured directly or through broader capital-market exposure, is materially lower and varies significantly by member state; Eurostat and EFAMA both show wide cross-country dispersion and a much stronger reliance on deposits in many markets. The available data consistently indicate a substantial participation gap between the U.S. and the EU.

Germany and France, two of the EU’s largest economies, are frequently cited as showing equity participation rates that trail US equivalents by a material margin, though the precise gap varies by source and methodology.

Multiple factors drive this gap: cultural attitudes toward investment, pension system structures, and historical market development. Regulatory access friction is a documented contributor, too. Narrower instrument availability, higher access costs, and leverage caps that make certain strategies unviable all reduce the incentive to participate.

Regulatory Asymmetry and Capital Flow Consequences

The US Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) impose their own retail trading restrictions.

In forex, for example, the CFTC caps leverage for US retail clients at 50:1 for major pairs, which is actually tighter than ESMA’s 30:1 limit in that specific context. For equities, structured products, and ETF access, however, US retail clients enjoy considerably broader access than their EU counterparts.

The consequence is a flow of both capital and talent toward US markets. EU-based asset managers, brokers, and increasingly retail traders themselves are structuring their activity to access US market infrastructure, either directly or through instruments that replicate US market exposure. The EU’s Capital Markets Union initiative, an ongoing project aimed at deepening and integrating EU capital markets, is explicitly designed to address this dynamic, but progress has been slow and fragmented across member states.

The EU is competing against the US for capital and market participation, and its current regulatory framework makes that competition harder. That’s a structural observation, not a political one.

So is there anything the EU is actually getting right?

The Case for the Defence: What EU Regulation Gets Right

Before writing off EU regulation entirely, consider what it’s actually trying to do and where the evidence suggests it’s succeeding.

Investor Protection Outcomes vs. US Retail Loss Data

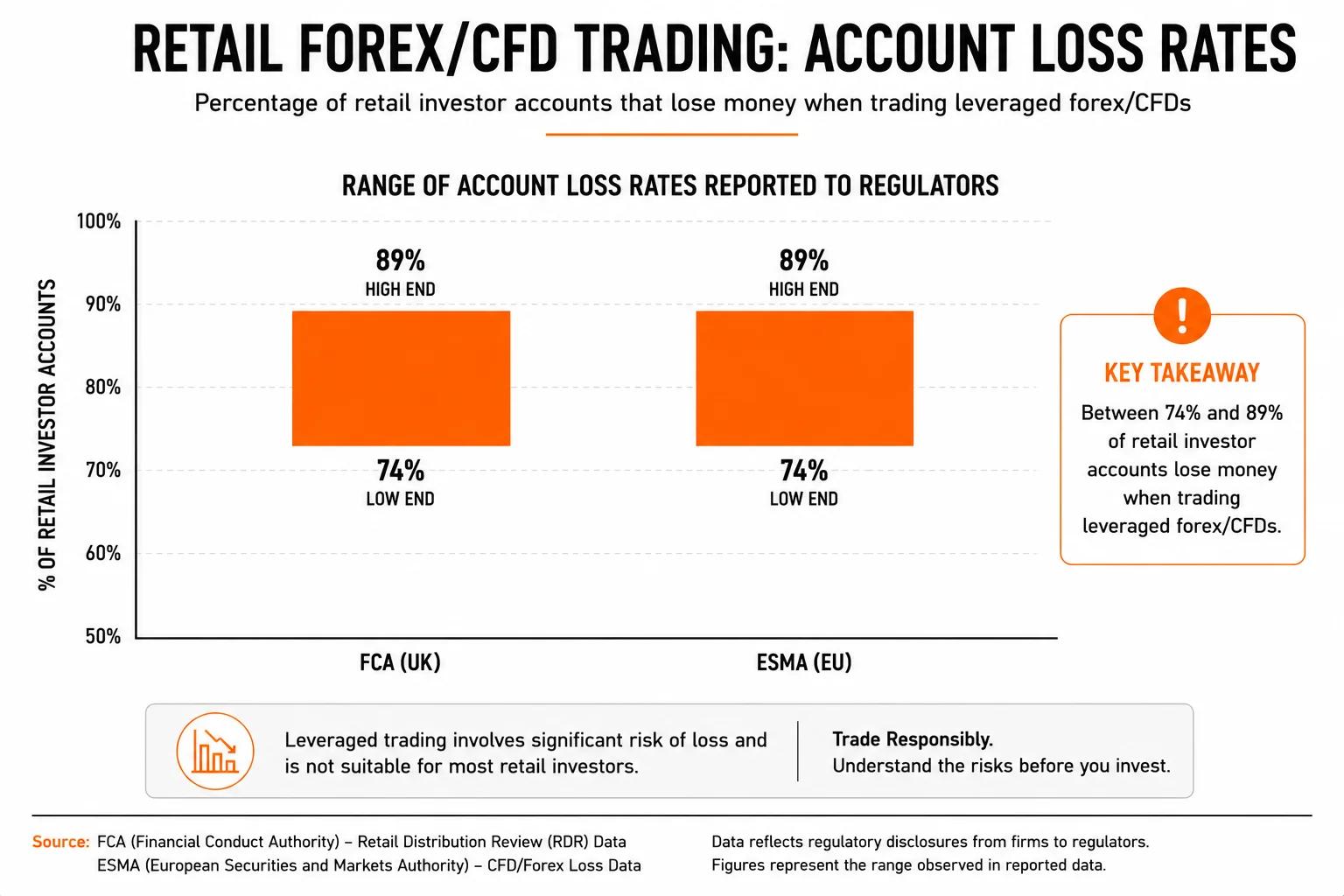

The leverage caps ESMA introduced exist for a reason. CFD providers operating in the EU were, before 2018, required to disclose the percentage of retail clients losing money. Those numbers were stark. According to ESMA’s March 2018 press release, citing analyses across EU national competent authorities, retail client loss rates on CFD trading ranged from 74% to 89% across major brokers.

Following ESMA’s intervention, there is indicative evidence that reduced leverage moderated the severity, if not always the frequency, of retail client losses, particularly in high-velocity instruments where excessive leverage accelerated drawdowns. The US has no equivalent mandatory disclosure regime for retail CFD or forex loss rates, making direct data comparison difficult. The CFTC data that does exist on retail forex dealer profitability consistently shows the majority of retail accounts losing money.

Excessive leverage tends to amplify losses faster than it amplifies gains. That is the core problem ESMA’s caps are designed to address. The constraints are real for traders who understand leverage management, but the underlying rationale is grounded in the pre-2018 loss data.

Where MiFID II Has Improved Market Transparency

MiFID II’s best execution requirements, transaction reporting mandates, and research unbundling rules have produced measurable improvements in market transparency for EU retail participants.

Specifically:

- Trade reporting granularity has increased, giving regulators and market participants better visibility into where and how trades are being executed.

- Research quality in some segments has improved, as the cost of producing low-quality research bundled into commissions was eliminated.

- Execution quality reporting (RTS 27 and 28 under MiFID II) gave retail clients a standardised basis for comparing broker execution quality for the first time.

If you’ve ever wondered whether your broker was actually getting you the best available price, MiFID II created a framework that at least requires them to demonstrate they’re trying.

The honest picture, then, is mixed, which brings us to the central question.

The Verdict: Overregulation, Underperformance, or Both?

EU financial regulation is not overregulation in intent, but it is overregulation in effect for a significant portion of retail traders.

The investor protection logic behind ESMA leverage caps and MiFID II compliance requirements is sound. The execution has produced real consumer welfare gains in some areas. The aggregate effect on EU retail market participation, broker diversity, and product accessibility is negative, though, and the EU’s own Capital Markets Union project implicitly acknowledges this by attempting to remedy the structural competitiveness gap it has identified.

EU regulation was designed primarily for consumer protection, with insufficient attention to how compliance costs, product restrictions, and access barriers would suppress retail market participation at scale. The US regulatory framework, for all its gaps, has produced a retail market ecosystem that is deeper, more diverse, and more accessible. EU regulators are aware of this. Closing the gap without dismantling the protections that do work is a genuinely difficult policy problem, not a simple case of Brussels bureaucracy run amok.

For you as a retail trader, the rules are working against your flexibility, if not necessarily against your long-term interests. How much that trade-off matters depends on your trading style, your risk profile, and what alternatives you’re willing to explore.

Practical Implications for Retail Traders in Europe

Understanding the regulatory landscape is useful. Knowing what you can do about it is better.

If you’re a retail trader based in the EU, your main options break down as follows:

Option 1: Trade within ESMA rules via an EU-regulated broker

This is the default position. You’re covered by EU investor protection frameworks, including negative balance protection, fund segregation requirements, and access to compensation schemes such as the Investor Compensation Company in Cyprus, which covers CySEC-regulated brokers up to EUR 20,000. The trade-off is the leverage caps and product restrictions described above. Comparing the best brokers for European traders gives you a structured starting point for comparing what’s available within this framework.

Option 2: Apply for professional client reclassification

Under MiFID II, retail clients can request reclassification as professional clients if they meet at least two of three criteria:

- You have carried out an average of at least 10 transactions of significant size per quarter over the previous four quarters.

- Your financial instrument portfolio (including cash deposits) exceeds EUR 500,000.

- You work or have worked in the financial sector for at least one year in a position requiring knowledge of the transactions or services in question.

Professional client status removes ESMA leverage caps and expands product access. It also removes some retail protections. Negative balance protection, for example, may no longer apply. Eligibility is specific, the application process involves your broker’s assessment, and the decision is theirs to make. If you meet the thresholds, it’s worth exploring, but it’s not a shortcut available to most retail participants.

Option 3: Access markets via non-EU or offshore brokers

Some EU-based traders open accounts with brokers regulated outside the EU, in jurisdictions such as the UK (post-Brexit), Australia (ASIC-regulated), or further afield. These brokers operate under different leverage and product rules and may offer access to instruments unavailable via ESMA-regulated brokers.

This is legal in most EU member states for individual retail clients accessing foreign services. In practical terms, it means stepping outside EU investor protection frameworks. Your funds may not be covered by EU compensation schemes, negative balance protection may not apply, and dispute resolution would be subject to the laws of the broker’s jurisdiction rather than EU law. If a broker operating outside EU regulation fails or acts against your interests, your recourse is meaningfully different. That’s a real consideration, not a reason to avoid non-EU brokers categorically, but it should inform how much capital you place with them and how carefully you select them.

For context on CFD trading and leverage mechanics before you compare conditions across jurisdictions, make sure you understand what you’re actually comparing. If you’re weighing up ESMA-regulated brokers against offshore alternatives, the protection differences are as important as the leverage differences.

This article is informational and does not constitute financial or legal advice. Your individual circumstances, including your tax residence, risk profile, and trading objectives, should be assessed with appropriate professional guidance before making decisions about where or how you trade.

Frequently Asked Questions

What is ESMA and why does it have authority over my trading?

ESMA, the European Securities and Markets Authority, is the EU's financial markets regulator, established under EU law. It has the authority to issue product intervention measures that apply across all EU member states, which means any broker regulated in the EU must comply with ESMA's rules regardless of which country within the EU they're based in. The leverage caps introduced in 2018 are an example of ESMA using this authority directly.

How does MiFID II actually affect my day-to-day trading conditions?

MiFID II primarily affects you through the requirements it imposes on your broker, which then shape what you can access and how. It's the reason your broker sends you execution quality reports, requires you to pass a knowledge assessment before trading CFDs, and asks about your trading experience during onboarding. The research unbundling rules under MiFID II are less directly visible but have changed how market analysis is produced and distributed.

Can I legally use a non-EU broker if I'm based in the EU?

In most EU member states, yes. Individual retail clients can generally access financial services from brokers based outside the EU. What changes is your protection framework. You lose access to EU investor compensation schemes, EU-mandated negative balance protection, and the enforcement mechanisms of EU financial law. The broker's regulatory jurisdiction governs the relationship. Verify the legal position in your specific country of residence before proceeding.

What is professional client status and who actually qualifies for it?

Professional client status under MiFID II removes ESMA leverage caps and some product restrictions. To qualify, you need to meet at least two of three criteria: a sufficient trading history (10 significant transactions per quarter over the past year), a financial instrument portfolio exceeding EUR 500,000, or relevant professional experience in financial services. Your broker conducts the assessment. Most retail traders will not meet two of those criteria, and the protections you give up, including negative balance protection, are worth factoring into the decision carefully.

Are EU stock markets actually underperforming relative to the US?

Over the past decade, yes, in terms of index returns, market capitalisation growth, and retail participation rates. The STOXX Europe 600 has materially underperformed the S&P 500 over most relevant time horizons. The causes are multiple, including sector composition differences (EU indices are heavier in financials and industrials, while the S&P 500 has benefited enormously from US tech dominance), as well as the structural and regulatory factors discussed in this article. Attributing the gap entirely to regulation would be an oversimplification, but regulation is a contributing factor.

What is the Capital Markets Union and does it change anything for retail traders?

The Capital Markets Union (CMU) is an EU initiative aimed at deepening and integrating European capital markets to reduce fragmentation and improve competitiveness relative to the US. It covers areas including retail investor access, cross-border investment barriers, and insolvency frameworks. Progress has been incremental rather than transformational. CMU-related reforms could eventually ease some of the product access restrictions described in this article, but meaningful change has been slow and the timeline for material retail impact remains unclear.

Do these rules apply to UK traders after Brexit?

Not in the same form. Since the UK left the EU, UK traders are governed by the Financial Conduct Authority (FCA) rather than ESMA. However, the UK retained its own PRIIPs-equivalent obligations post-Brexit, and UK retail clients faced broadly similar practical restrictions on access to US-listed ETFs for most of the post-Brexit period. The UK's Consumer Composite Investments (CCI) regime, which replaces PRIIPs, became effective in April 2026 with mandatory application from June 2027. [FACT-CHECK REQUIRED: legal review recommended to confirm current retail access position and accurate CCI implementation dates before publication.] UK traders are no longer covered by EU investor compensation schemes or EU-level dispute resolution mechanisms. The UK's regulatory trajectory post-Brexit is its own developing story.

About the authors

Related articles

How Much Do Forex Traders Actually Make? A Realistic Income Breakdown

A realistic, data-grounded breakdown of forex trader income across four trader types, from part-time retail to institutional, including what account size actually means for your earnings.

Which Forex Brokers Have the Most Complaints? What Regulatory Records Actually Show

Learn how to check forex broker complaint records across FCA, ASIC, NFA, and CySEC databases; and what those records actually tell you before you open an account.

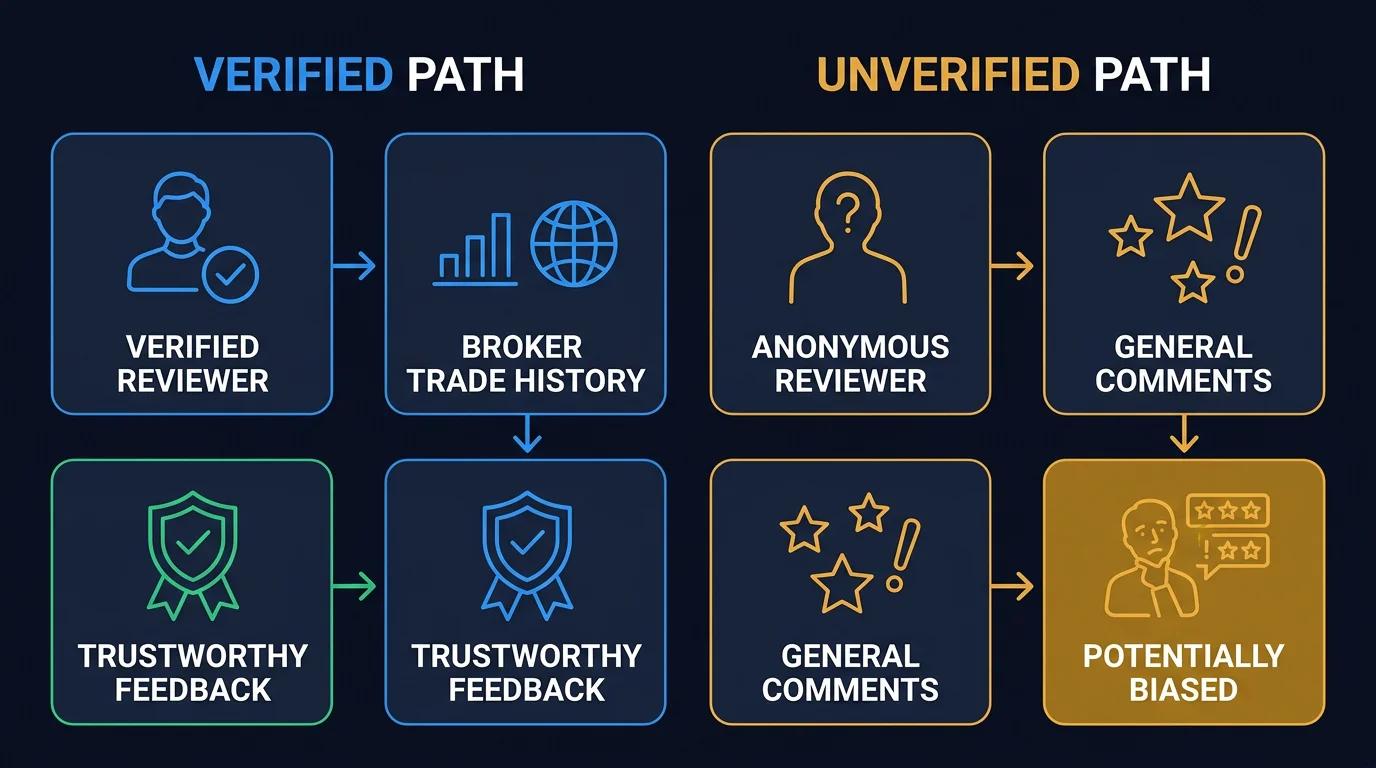

Verified vs Unverified Forex Broker Reviews: What the Difference Actually Means

What "verified" actually means on broker review platforms, how to spot fake review campaigns, and how to build a credibility framework that surfaces genuine signal before you open an account.

0 comments