Trading Strategies · Beginner · 10 min read

Dollar-Cost Averaging Explained: Mechanics, Benefits and Real Performance Data

Dollar-cost averaging is an investment discipline where you invest a fixed amount of money at regular intervals, regardless of the asset's price. It spreads your entry across different price levels, removes the pressure to time the market, and turns a volatile chart into a mechanical schedule. For retail traders, DCA reduces emotional decisions and enforces consistency.

What is dollar-cost averaging and how does it work

Dollar-cost averaging (DCA) is the practice of dividing a total investment into equal instalments and buying at fixed intervals, weekly, monthly or quarterly, regardless of the asset's current price. Commit £500 a month to a global equity ETF (an exchange-traded fund is a basket of securities traded on an exchange like a single stock), and the calendar decides your entries, not your emotions. The strategy is agnostic about direction: you buy the same currency amount in bull runs, corrections and sideways drift.

The mechanics are simple but the effect is subtle. Because you invest a fixed cash amount rather than a fixed number of shares, you automatically buy more units when prices fall and fewer when prices rise. Over a full cycle, your average cost per share tends to be lower than the arithmetic mean of prices during the period. That property is often called the harmonic mean effect, and it is the mathematical backbone of the entire strategy.

DCA does not predict tops or bottoms nor guarantee gains. What it does is convert an ambiguous question, when should I invest, into a policy: on the first business day of every month, transfer this amount, buy this instrument. That policy is what most retail traders lack, and it is often more valuable than any signal or indicator on your chart. Understanding position sizing in trading helps reinforce this discipline, since each fixed investment amount becomes your position size rule.

How dollar-cost averaging reduces the impact of volatility

When you invest the same amount every month, price volatility works in your favour rather than against you. Falling prices mean each instalment buys more units; rising prices mean each instalment buys fewer. Your average purchase price gets pulled below the simple average of the market's quoted prices during the period. Volatility, which most retail investors experience as stress, becomes an ingredient in a lower cost basis.

The second effect is behavioural. A 20% drawdown (a drawdown is the fall from a capital peak to the trough before a new peak) is painful in a lump-sum portfolio because every pound was committed at the pre-crash price. In a DCA schedule, the same drawdown means your next scheduled purchase buys at a discount, which reframes the loss as an opportunity. Beginner trading lessons from 10 years in the markets often highlight how this reframing separates traders who abandon their plan during corrections from those who stay disciplined.

| Market pattern | Impact on DCA outcome | Impact on lump sum |

|---|---|---|

| Steady uptrend | Positive, but capped by staggered entry | Best case, full exposure early |

| Sharp drawdown then recovery | Favourable, low average cost | Painful drawdown on full stake |

| Sideways with volatility | Advantage from harmonic mean | Neutral to slightly negative |

| Prolonged downtrend | Losses smaller than lump sum | Worst case |

Dollar-cost averaging versus lump-sum investing: what the research shows

Academic and industry research consistently finds that lump-sum investing beats DCA in the majority of historical market windows, because markets rise more often than they fall. Vanguard's 2012 paper 'Dollar-cost averaging just means taking risk later' analysed rolling 10-year periods across US, UK and Australian markets and reported that lump-sum investing outperformed DCA in roughly two-thirds of periods, with a wider margin the longer the horizon.

The intuition is straightforward: if the expected return of the asset is positive, keeping cash uninvested during a DCA schedule imposes an opportunity cost. Every month you have not yet deployed is a month of missed expected return. In a market that drifts upward on average, delaying deployment is mathematically expensive.

DCA wins in three specific contexts.

- First, prolonged bear markets or extended sideways ranges, where lump-sum entries suffer the full drawdown while DCA lowers the average cost.

- Second, portfolios where you do not have a lump sum available and are investing from monthly income, which is the situation of most retail traders.

- Third, cases where the psychological cost of a badly timed lump sum, freezing you for years, exceeds the expected-return advantage. For many retail investors, passive income for beginners through regular DCA contributions is the most realistic path to building wealth without the pressure of perfect timing.

The honest framing is that lump-sum investing has better expected returns, and DCA has better worst-case behaviour. Which one suits you depends on your capital source, your risk tolerance and how you have reacted to past drawdowns.

Real-world DCA example: investing £500 monthly over twelve months

Consider a trader who invests £500 on the first of every month into a UK-listed ETF for twelve months while the price per share fluctuates between £40 and £60. Total outlay is £6,000. In a month with a £40 price, £500 buys 12.5 shares; in a month at £60, £500 buys 8.33 shares. Cheap months contribute more units to the running total than expensive months.

| Month | Share price | Shares bought | Cumulative shares |

|---|---|---|---|

| 1 | £50 | 10.00 | 10.00 |

| 2 | £45 | 11.11 | 21.11 |

| 3 | £40 | 12.50 | 33.61 |

| 4 | £42 | 11.90 | 45.51 |

| 5 | £48 | 10.42 | 55.93 |

| 6 | £55 | 9.09 | 65.02 |

| 7 | £60 | 8.33 | 73.35 |

| 8 | £58 | 8.62 | 81.97 |

| 9 | £52 | 9.62 | 91.59 |

| 10 | £47 | 10.64 | 102.23 |

| 11 | £50 | 10.00 | 112.23 |

| 12 | £53 | 9.43 | 121.66 |

The arithmetic mean of the twelve monthly prices is £50.00, but the DCA average cost is £6,000 divided by 121.66 shares, roughly £49.32. The gap is small in this example but grows in more volatile assets. This is the harmonic mean effect at work, and it is why disciplined DCA appeals to traders who value predictable entry mechanics over forecasting.

Psychological and risk management benefits of regular investing

DCA removes the emotional burden of choosing when to invest by outsourcing the decision to a calendar. You never face the question 'is this the top', because the answer, whatever it is, does not change your next scheduled purchase. You sidestep the paralysis of waiting for a better entry that may never come, and you avoid the regret of committing a lump sum days before a correction.

From a behavioural finance perspective, DCA neutralises two of the most costly biases in retail trading: anchoring on recent prices, and loss aversion. Anchoring makes you refuse to buy because 'it was cheaper last week', which delays deployment indefinitely. Loss aversion makes you sell in panic when the portfolio is red. A rigid DCA schedule ignores both signals and, over multi-year horizons, that indifference is a feature.

DCA also enforces position sizing implicitly. Because each purchase is a fixed cash amount, no single entry can dominate the portfolio's cost basis. For traders prone to overtrading, chasing green candles with oversized market orders, DCA acts as a circuit breaker.

DCA with cryptocurrencies and alternative assets

Dollar-cost averaging is particularly popular in cryptocurrency because volatility is extreme and timing is close to impossible. Investors accumulate Bitcoin or Ethereum by scheduling weekly or monthly buys of fixed fiat amounts, smoothing entries across cycles that can move 50% in either direction within weeks. The harmonic mean effect is proportionally larger in crypto than in equities, precisely because dispersion is higher. Our crypto trading guide covers the mechanics of spot purchases and the regulatory landscape that affects UK retail traders.

The FCA has prohibited the sale of crypto-derivative products (including CFDs on cryptoassets) to UK retail clients since January 2021, a rule reconfirmed in the FCA's 2023 financial promotions regime. UK retail traders cannot DCA into crypto via CFD accounts, but spot purchases of cryptoassets through FCA-registered exchanges remain available, subject to the marketing restrictions and risk warnings the FCA imposes.

FCA, 2021 policy statement PS20/10: The FCA banned the sale of derivatives and exchange-traded notes referencing certain cryptoassets to UK retail consumers, effective 6 January 2021.

Beyond crypto, DCA works with commodities ETFs, REITs (real estate investment trusts), and thematic funds. It does not work well with instruments that carry a holding cost, such as leveraged CFDs with overnight financing, because the swap charges compound while you accumulate. If an instrument bleeds every night you hold it, staggering entries only extends your exposure to that bleed.

Tax efficiency and DCA: what you need to know

DCA can improve tax efficiency in the UK because regular small purchases fit naturally within annual tax-sheltered allowances. HMRC sets the ISA (Individual Savings Account) subscription limit at £20,000 per tax year as of the 2024 to 2025 tax year, and monthly instalments of up to £1,666 automatically stay inside that envelope, sheltering gains and dividends from capital gains tax and income tax.

Outside an ISA, staggered purchases create a cleaner cost-basis audit trail. Each instalment is a separate acquisition with a timestamp and price, which simplifies section 104 pooling calculations for UK capital gains tax and equivalent rules elsewhere. This is not tax advice: rules on same-day and 30-day matching, and on the annual CGT allowance (£3,000 for 2024 to 2025), can change the outcome, and you should consult a tax adviser for your circumstances.

Automated DCA platforms and robo-advisors

Modern investment platforms automate DCA by scheduling recurring purchases and, in some cases, rebalancing the portfolio on a set calendar. You configure the amount, the frequency and the target holdings once, and the platform executes without further input. This removes the last friction point in the strategy, remembering to place the order, and closes the gap between plan and execution.

| Platform type | Typical DCA feature | Typical UK retail fit |

|---|---|---|

| Robo-advisor | Recurring deposit plus auto-rebalance | ISA and general accounts |

| Stockbroker with regular investing | Scheduled ETF and share purchases at reduced commission | ISA, SIPP and GIA |

| Regulated crypto exchange | Recurring spot buys of major cryptoassets | Spot only, no CFDs for UK retail |

When you evaluate a platform for DCA, check three things.

- First, the entity that onboards you and its authorisation: an FCA-authorised firm (Financial Conduct Authority, the UK regulator) is the gold standard, and offshore group entities should be treated as a lower tier.

- Second, the fee structure on small recurring trades, since flat commissions can dominate returns on £100 monthly buys.

- Third, whether the platform supports the tax wrapper you need, typically an ISA or SIPP for UK residents. Best investments for passive income provides a framework for evaluating platforms and asset selection alongside your DCA schedule.

Frequently Asked Questions

Is dollar-cost averaging better than investing a lump sum all at once?

On expected return, lump-sum investing wins about two-thirds of the time historically, according to Vanguard's rolling-period analysis across US, UK and Australian markets. On worst-case outcomes and behavioural stability, DCA is safer. If you have a lump sum, high risk tolerance and a long horizon, lump sum is mathematically preferred. If you invest from monthly income or fear catastrophic timing, DCA is the more practical choice.

Can I use dollar-cost averaging with stocks, ETFs, and cryptocurrencies?

Yes for stocks and ETFs, and yes for spot crypto through regulated exchanges. In the UK, retail clients cannot DCA into crypto via CFDs because the FCA banned crypto-derivative sales to retail from January 2021. DCA works poorly with leveraged CFDs on any asset, because overnight financing costs accumulate while you hold the position.

How often should I invest using dollar-cost averaging: weekly, monthly, or quarterly?

Monthly is the default for most retail traders because it aligns with salary cycles and keeps transaction costs proportionate. Weekly can suit crypto and higher-volatility assets, where more frequent buys capture more of the harmonic mean effect. Quarterly reduces friction but leaves too much cash idle. Match the frequency to your cash flow and to the platform's commission on small recurring trades.

Does dollar-cost averaging guarantee profits or protect me from losses?

No. DCA lowers your average cost during volatile periods and reduces the worst-case outcome of poor timing, but it cannot make a losing asset profitable. If the underlying instrument trends down for the whole holding period, DCA will still show a loss, just a smaller one than a lump sum entered at the peak. It is a discipline, not a hedge.

What is the difference between dollar-cost averaging and value averaging?

DCA invests a fixed cash amount every period regardless of price. Value averaging invests a variable amount to hit a fixed portfolio value target every period, buying more when the portfolio is below target and less, or nothing, when above. Value averaging can produce a lower average cost in theory but demands larger cash reserves and more active management, which erodes its practical appeal for most retail traders.

About the authors

Related articles

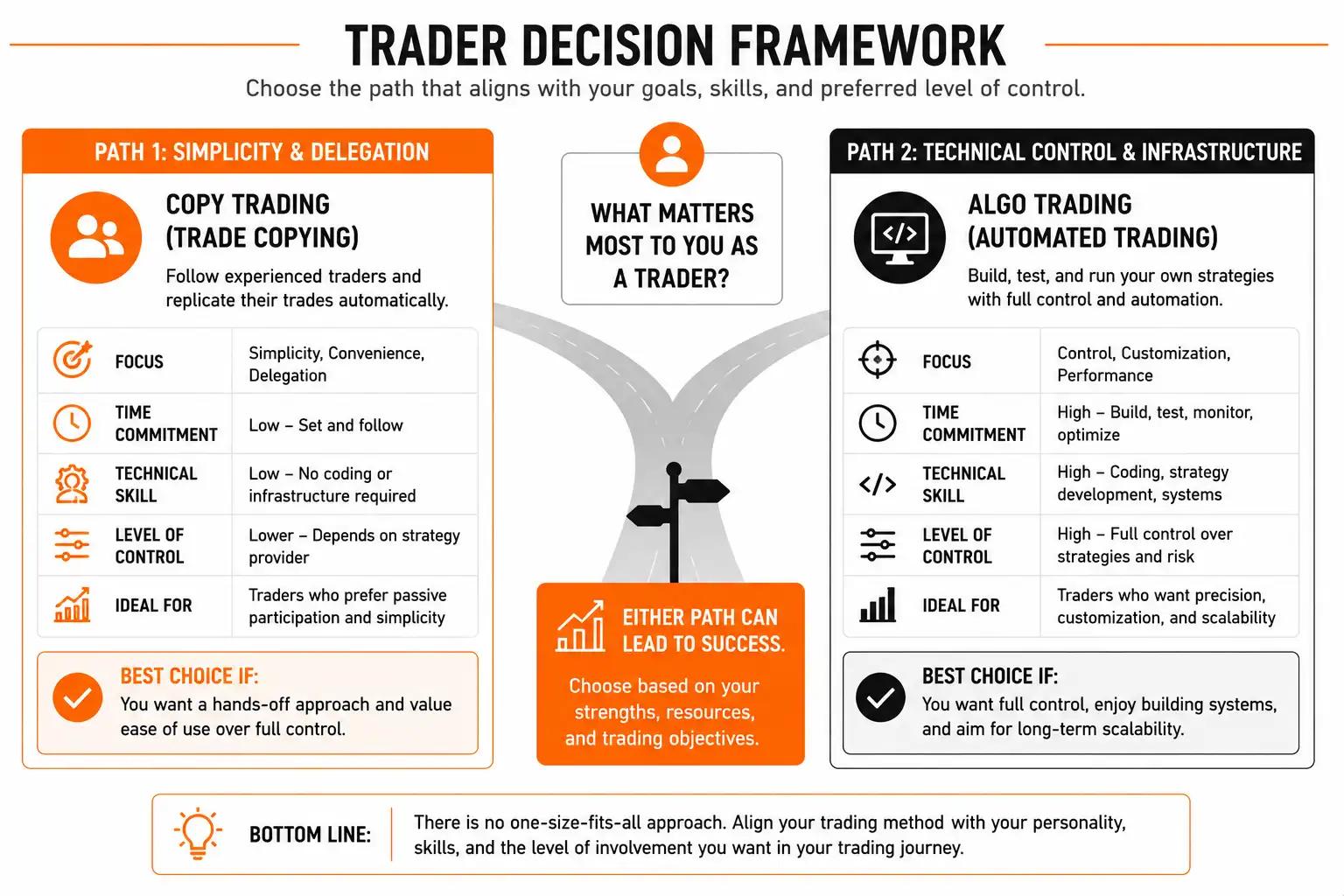

Copy Trading vs Algo Trading: Which Has the Better Risk Profile?

Discover how copy trading and algo trading differ in risk profile, who controls the risk, and which approach suits your trading style.

5 Trading Strategies That Work Across Multiple Asset Classes

Discover trading strategies that work across forex, stocks, indices, and commodities; with clear guidance on how to adapt each one.

Breakout Trading Strategy: How to Identify Real Breaks From False Ones

Learn the breakout trading strategy and how to spot real breaks from false ones using volume, confirmation, and clean entry rules that protect your capital.

0 comments