The best passive income vehicles for you as a retail investor are dividend stocks, bonds, and real estate (direct or via REITs), plus peer-to-peer lending, and diversified funds. Each demands different capital, patience, and risk tolerance; tax treatment varies by jurisdiction. Pick the mix that fits your runway, not the highest headline yield.

What are the best investments for passive income?

Passive income is money you earn without daily active work once the asset or system is in place. For most retail investors, the best investments for passive income cluster around three anchors: dividend-paying equities, bonds, and real estate, either direct or through REITs (a real estate investment trust is a listed vehicle that owns income-producing property and distributes most of its profits to shareholders). Around those anchors sit newer options: peer-to-peer lending, and crypto staking.

No option is truly hands-off. Dividend portfolios need periodic rebalancing. Bonds require reinvestment as they mature. Rental property involves tenants, repairs, and vacancy risk. Peer-to-peer loans need diligence on the platform and the borrower profile.

The right mix depends on three variables: how much capital you can commit, how long you can wait for cash flow, and how much drawdown (the fall from a capital peak to the trough before a new peak) you can absorb without abandoning the plan. According to ESMA's 2024 CFD intervention review, between 74 and 89% of retail CFD accounts lose money, which is one reason many retail investors prefer income-first strategies over leveraged trading.

Dividend stocks and investment funds

Dividend-paying stocks and funds distribute part of company profits to shareholders, typically quarterly, offering both income and possible capital appreciation. A dividend is a cash payment per share; the dividend yield is the annual payment divided by the share price. Dividend aristocrats, companies that have raised payouts for 25 or more consecutive years, provide a screened starting point for income-focused portfolios because the consistency filter removes most speculative names.

Funds simplify the process. Dividend ETFs (exchange-traded funds, listed baskets of stocks bought and sold on an exchange) pool payouts from dozens or hundreds of companies and pay you a proportional distribution. This spreads single-company risk at the cost of a small management fee, usually expressed as the total expense ratio (TER).

For UK retail investors, dividend income received inside a Stocks and Shares ISA is free of UK income tax and capital gains tax on gains, according to HMRC guidance (as of April 2026). Outside a wrapper, dividends above the annual allowance are taxed at rates that depend on your income band. Broker choice is also important since some UK brokers charge FX conversion fees of 0.5 to 1.5% on US-listed dividend stocks, which erodes yield over time.

Bonds and fixed-income securities

Bonds pay fixed interest at regular intervals and return principal at maturity, which makes them predictable income sources with lower volatility than equities. A coupon is the periodic interest payment; the yield to maturity blends coupon and price movement into a single annualised return figure. Government bonds (such as UK gilts or US Treasuries) sit at the safest end. Investment-grade corporate bonds pay more; high-yield or 'junk' bonds pay the most but carry meaningful default risk.

Bond funds and bond ETFs let you diversify across dozens of issuers without buying individual securities, which matters because a single corporate default can wipe out years of coupon income on a concentrated position. Duration (a measure of how sensitive a bond's price is to interest rate changes, expressed in years) is the risk lever most retail investors underestimate: a 10-year bond loses roughly 10% of its price for every 1% rise in yields.

As of April 2026, UK gilts and short-dated Treasuries have offered yields in the 4 to 5% range, according to the Bank of England and US Treasury data. That competes directly with dividend yields, so bonds have re-entered mainstream income portfolios after a decade of near-zero rates.

Real estate and rental property income

Rental properties generate monthly tenant payments that can exceed mortgage and maintenance costs, building equity while producing cash flow. The catch is capital intensity: a UK buy-to-let typically needs a 25% deposit, plus stamp duty, legal fees, and cash reserves for voids and repairs, according to UK Finance data (2024). Net yield after mortgage interest, agent fees, insurance, and maintenance is often 3 to 5%, well below the gross rental yield advertised by agents.

Real estate investment trusts (REITs) offer property exposure without direct management. A REIT is a listed vehicle that owns income-producing real estate and, in most jurisdictions, must distribute at least 90% of taxable income to shareholders. That structure creates high dividend yields, typically 4 to 8%, but REITs trade like stocks and can fall 30 to 50% in a market crash, as they did in 2020 and 2022.

Peer-to-peer lending and crowdfunding platforms

Peer-to-peer (P2P) lending platforms connect borrowers and lenders directly, letting you earn interest on loans; crowdfunding platforms let you invest in startups or property projects for equity or debt returns. Advertised P2P yields typically sit between 5 and 12%, but headline rates ignore defaults, platform failure risk, and the loss of FSCS protection: P2P investments are not covered by the £85,000 UK deposit compensation scheme, according to the FCA.

Equity crowdfunding on platforms such as Seedrs or Crowdcube gives you shares in early-stage companies. The base rate is failure: the British Business Bank reported that around 60% of early-stage startups do not return capital. Tax reliefs under EIS and SEIS partially offset losses for UK investors, but liquidity is effectively zero for five to ten years. Treat P2P and crowdfunding as satellite positions, not core holdings.

Tax implications and diversification strategy

Passive income is taxed by source: dividends and interest as ordinary income (with dividend allowances in some jurisdictions), capital gains at preferential rates in many countries, and rental income after allowable expenses and, in some regimes, depreciation. UK investors have the ISA (£20,000 annual limit as of April 2026) and SIPP wrappers to shelter dividends, interest, and gains, according to HMRC. Using wrappers first typically adds more to net income than chasing an extra percentage point of gross yield.

Diversification across asset classes reduces concentration risk and smooths the income profile. A portfolio built only on high-yield dividend stocks will drop 30 to 50% in a bear market alongside its payouts, as several 2020 examples showed. Mixing bonds, REITs, and cash-like instruments cushions the drawdown.

Source: HMRC guidance, tax year 2025 to 2026.

Comparing time-to-profitability across passive income methods

Dividend stocks and bonds start paying within weeks; rental properties take months to years before positive cash flow. Understanding the lag between initial investment and first returns helps you match strategies to your financial runway and monthly obligations. A trader with 6 months of expenses in reserve can wait for a course to compound; a saver who needs income next quarter should stay in dividends, bonds, and interest-bearing accounts.

One under-discussed route is automated trading, sometimes called algorithmic investing. Retail platforms such as MT4, MT5, and cTrader allow you to run an expert advisor (an EA is a script that opens and closes trades according to coded rules) on a live account. This is not truly passive: strategies decay, spreads widen in news events, and drawdowns can be sharp.

ESMA, 2024 CFD intervention review: Between 74 and 89% of retail CFD accounts lose money across EU-regulated brokers, a headline figure that underpins the case for income-based rather than leveraged strategies.

Frequently Asked Questions

How much capital do you need to start earning passive income from investments?

You can start with £100 or less in dividend ETFs, REITs, and government bond funds through most UK brokers. Meaningful monthly income needs more: a 4% net yield generates £333 per month from £100,000 invested. Direct rental property typically requires at least £40,000 for a deposit in most UK regions, according to UK Finance data. Start small in liquid instruments while you learn the tax and risk profile.

What is the difference between passive income and active trading returns?

Passive income comes from assets or systems that pay you without constant intervention: dividends, coupons, rent, licensing fees. Active trading returns come from opening and closing positions frequently, and require ongoing time, focus, and risk management. According to ESMA (2024), 74 to 89% of retail CFD accounts lose money, which highlights why passive strategies are the more common route to durable income.

Can you combine multiple passive income streams, and should you?

Yes, and diversification across streams is one of the most reliable ways to smooth income. A common structure is 60 to 70% in dividend and bond funds inside an ISA or SIPP, 15 to 25% in REITs or direct property, and a smaller satellite in digital products or P2P lending. This spreads market, credit, and platform risk while keeping tax efficiency intact.

What are the main risks of passive income investments, and how do you manage them?

The main risks are market drawdown (equities and REITs), interest rate risk (bonds), tenant and vacancy risk (property), platform and default risk (P2P), and effort risk (digital products that never gain traction). Manage them with diversification across asset classes, position sizing, use of tax wrappers, and cash reserves that let you avoid selling into a downturn.

How does geographic location affect which passive income investments are available to you?

Jurisdiction determines tax wrappers, product access, and platform regulation. UK investors have ISAs, SIPPs, and FSCS-protected cash savings; US investors have Roth IRAs and 401(k)s; EU investors face MiFID II product restrictions. Some P2P and crypto staking platforms are unavailable to UK retail clients under FCA rules. Always confirm the entity that onboards you and the licence it holds before depositing.

About the authors

Related articles

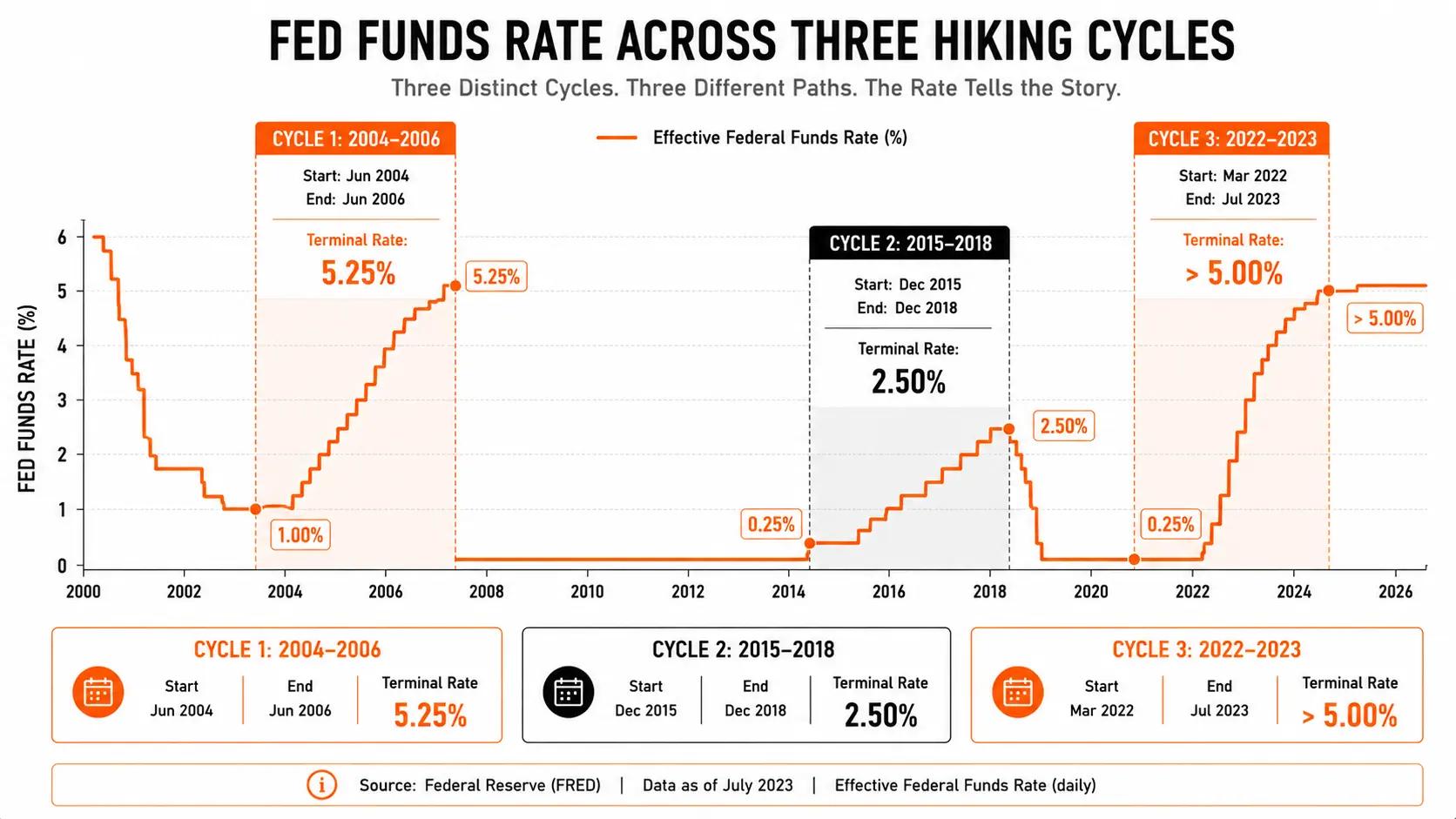

Which Asset Classes Perform Best During Rate Hiking Cycles?

Historical performance of equities, bonds, commodities, real estate, and currencies during Fed and ECB rate hiking cycles; with patterns, caveats, and a framework for using the data.

Passive Income for Beginners: A Realistic Guide to Your First Stream

Passive income for beginners explained: startup costs, timelines, tax rules by jurisdiction, risk assessment and the automation tools that keep streams running.

Popular American ETFs and Their European Equivalents

Can't buy SPY or QQQ in Europe? Find the closest UCITS ETF for each major US fund, with costs, tickers, and key differences explained.

0 comments