Investing · Beginner · 10 min read

Passive Income for Beginners: A Realistic Guide to Your First Stream

Passive income for beginners is money you earn with minimal ongoing effort after an upfront investment of time, capital, or both. Unlike a salary, it keeps paying when you stop working. Realistic first streams include dividend stocks, index funds, and rental property, each with different startup costs, timelines, and risks.

What Is Passive Income for Beginners

Passive income is a stream of earnings that continues with limited day-to-day involvement once you have done the initial work or committed the capital. For a beginner, the phrase covers everything from a dividend paid quarterly on a share you own to rent from a property. The defining feature is the ratio: hours worked today versus pounds received next month. Active income requires you to trade time for money on a rolling basis; passive income decouples the two after a heavier upfront push.

The common misconception is that passive means effortless. It is not. Every genuine passive income method demands one of three inputs at the start: money, time, or expertise. A dividend portfolio needs capital. A blog needs months of writing. A rental property needs both a deposit and administration. What changes over time is the maintenance load, not the initial workload. Useful mental test: after month three, does the income continue if you disappear for a fortnight. If yes, the stream is genuinely passive. If it collapses without you, it is a side business.

For beginners the practical goal is building the first stream to a stable, automated state, then adding a second. Compounding, diversification and tax efficiency do the heavy lifting over years.

Passive Income Ideas Ranked by Startup Capital Required

Passive income methods sit on a spectrum from near-zero capital to five-figure commitments, and choosing by what you actually have is the fastest way to start.

A beginner with £200 and free evenings faces a different menu than one with £20,000 and a full-time job. The table below ranks common streams by the realistic minimum capital to begin, not the theoretical minimum quoted by platforms.

Low-capital methods tax your time and high-capital methods tax your patience. Content sites and digital products cost little in pounds but demand months of writing before a first payout. ETFs pay you within weeks but need meaningful capital to produce meaningful cash. Rental property sits at the top of the ladder: high entry, higher potential yield, meaningful administration.

How Long Before Passive Income Actually Pays You

Most passive income streams take months or years to produce a payout worth noticing, and the timeline depends far more on the method than on your effort. Dividend ETFs can pay their first distribution within a quarter of purchase, but a portfolio large enough to cover a phone bill takes years of contributions and reinvestment.

Rental property income begins after purchase, refurbishment and tenant placement, usually 3 to 6 months from offer accepted. Peer-to-peer lending pays interest monthly from the first funded loan, but principal recovery takes the full loan term.

The practical implication is to treat the first year as an investment phase. Reinvest every early payout back into the same stream. Compounding only works if you leave it alone.

Tax Implications and Reporting by Jurisdiction

Passive income is taxable in almost every jurisdiction, and the rate and paperwork depend on both the income type and where you are resident. Ignoring this at the start is one of the most expensive mistakes a beginner can make. In the UK, dividend income above the £500 annual allowance (as of the 2024 to 2025 tax year, per HMRC) is taxed at 8.75%, 33.75% or 39.35% depending on your income band. Rental income is added to your other income and taxed at your marginal rate, and you report it on the self-assessment return.

Interest from savings and peer-to-peer lending falls under the personal savings allowance (£1,000 for basic-rate taxpayers, £500 for higher-rate, per HMRC) before income tax applies.

In the US, the IRS classifies dividends as qualified or ordinary, with qualified dividends taxed at capital gains rates and ordinary dividends taxed as regular income. Rental income is ordinary income, reported on Schedule E. In Australia, the ATO treats most passive income as assessable income taxed at marginal rates, with franking credits available on Australian dividends.

Wrap tax-efficient accounts around your streams from day one where possible: a stocks and shares ISA in the UK shelters dividends and capital gains, and a SIPP defers tax on pension contributions. In the US, a Roth IRA offers tax-free growth within contribution limits.

Risk Assessment: Which Passive Income Methods Are Safest

Risk in passive income is a mix of capital loss risk, income volatility, liquidity risk and platform risk. A high-yield savings account carries almost no capital risk within FSCS protection limits (£85,000 per authorised institution in the UK) but pays a modest, inflation-sensitive return. A dividend ETF has capital loss risk if markets fall, but income tends to be steady from a diversified basket. Individual dividend stocks add concentration risk: a single company can cut its dividend or fail entirely.

Peer-to-peer lending carries default risk on the underlying borrowers and platform risk if the operator collapses. The FCA has repeatedly flagged peer-to-peer as high risk for retail investors and, since 2019, restricts non-sophisticated retail investors to 10% of their investable assets in this category. Buy-to-let property carries tenant risk, void periods, interest rate risk on the mortgage, and low liquidity: selling takes months. Cryptocurrency staking and yield products sit at the top of the risk stack; the FCA has banned the sale of crypto derivatives to UK retail clients and warns that investors should be prepared to lose all their money.

The practical rule for beginners is to build the base of the portfolio with cash savings and diversified funds, then layer higher-risk streams on top only with capital you can lose without pain. Diversification across at least three uncorrelated streams protects the whole portfolio when one fails.

FCA, 2024: UK retail investors are restricted from committing more than 10% of investable assets to high-risk investments including peer-to-peer loans and non-mainstream pooled investments.

Common Mistakes That Kill Passive Income Streams

Most passive income failures are caused by predictable beginner mistakes that compound over months.

- The first is expecting income before doing the work. Every passive stream has a J-curve: costs and effort come first, income arrives later.

- The second mistake is chasing yield. A savings account paying 10% when the base rate is 4% is not a bargain; it is a warning. Peer-to-peer platforms advertising 12% returns are pricing in a default rate you may not have modelled. Yield above the risk-free rate is compensation for risk you are taking, not a gift.

- The third is neglecting tax. Beginners often build a taxable dividend portfolio outside an ISA, pay avoidable tax for years, then discover the mistake when the position is too large to unwind cheaply. Use tax wrappers from pound one.

- The fourth is single-stream concentration. Relying on one property or one platform means one bad event ends your income. Diversify across at least three streams before you scale any of them.

- The fifth is failing to automate: manual rent collection, manual dividend reinvestment. Every manual step is a future point of failure.

- The sixth is not tracking. If you do not know what each stream earns net of costs and tax, you cannot tell which one deserves more capital.

Automation Tools to Manage Your Passive Income Streams

Automation is what separates a passive stream from a second job, and the tools you choose in month one shape how much of your time month twelve consumes. For investing, most UK brokers offer automatic dividend reinvestment (DRIP) and scheduled monthly contributions; turn both on the day you open the account. Portfolio trackers like Sharesight or the broker's own reporting handle tax paperwork at year end.

For rental property, letting agents or software like Landlord Studio automate rent collection, expense tracking and Making Tax Digital reporting to HMRC. Zapier and IFTTT connect the gaps between tools: a new sale on Gumroad can log itself into a spreadsheet, trigger a receipt and update your tax file in one flow.

Getting Started: Your First Passive Income Stream

The right first stream matches your current capital, skills and available hours. If you have £500 to £2,000 and limited time, open a stocks and shares ISA and buy a broad dividend or global index ETF, then set up a monthly standing order. Passive income for beginners with capital works best when the setup takes an evening and the maintenance takes an hour a quarter.

If you have time but little capital, start a niche affiliate site or a digital product in a subject you already understand. Expect 6 to 12 months before revenue. If you have both, add a REIT or peer-to-peer position within FCA guidance to diversify. Start with one stream. Automate it. Only add a second once the first runs itself.

Frequently Asked Questions

Can you really make passive income as a complete beginner with no money?

Yes, but you pay in time instead of capital. Content sites, YouTube channels, affiliate marketing and digital products can start for under £100, but they typically need 6 to 18 months of consistent work before revenue is meaningful. The trade-off is real: no capital means you invest hundreds of hours upfront in exchange for income later.

How much passive income do you need to replace a full-time job?

A common rule is 25 times your annual expenses invested in dividend or index assets, based on a 4% safe withdrawal rate. If you spend £30,000 a year, that suggests a portfolio of around £750,000. Property or business income can reduce this figure but adds management work, which makes the income less passive.

What is the difference between passive income and residual income?

Passive income requires little ongoing effort once established: dividends, rent, royalties. Residual income is a personal finance term for money left after essential expenses are paid, regardless of how you earned it. The terms are used interchangeably in marketing but mean different things in accounting and financial planning.

Is passive income legal and do you have to report it to tax authorities?

Passive income is legal in every mainstream jurisdiction and must be reported. In the UK, HMRC requires reporting of dividends above the annual allowance, all rental income, and interest above the personal savings allowance, usually through self-assessment. In the US, the IRS requires reporting on Schedule B, Schedule E and other forms depending on the source. Non-reporting attracts penalties and interest.

Which passive income method is best for someone under 30?

Time is the biggest advantage under 30, so methods that compound benefit most. A stocks and shares ISA holding a low-cost global index or dividend ETF, funded monthly, uses decades of compounding. Digital products or a content site pair well because early years allow experimentation without dependants relying on the income.

About the authors

Related articles

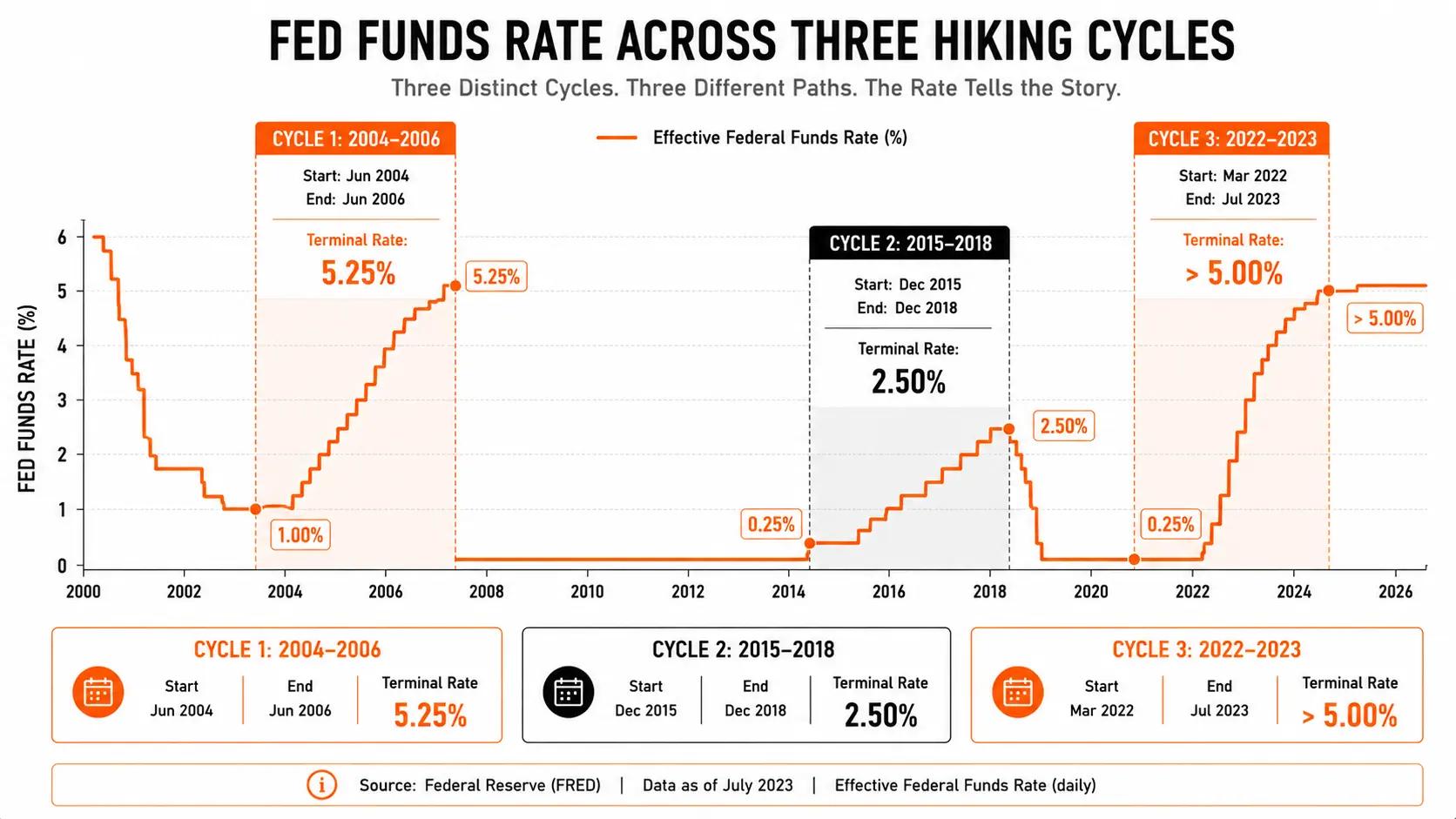

Which Asset Classes Perform Best During Rate Hiking Cycles?

Historical performance of equities, bonds, commodities, real estate, and currencies during Fed and ECB rate hiking cycles; with patterns, caveats, and a framework for using the data.

Best Investments for Passive Income: A Retail Investor's Playbook

A working guide to the best investments for passive income: dividends, bonds, real estate, digital products, P2P lending, plus a time-to-profitability comparison.

Popular American ETFs and Their European Equivalents

Can't buy SPY or QQQ in Europe? Find the closest UCITS ETF for each major US fund, with costs, tickers, and key differences explained.

0 comments