Questions to Ask Before Opening a Trading Account

This article is for informational purposes only and does not constitute financial advice. Regulatory rules and compensation limits vary by jurisdiction and are subject to change.

This article gives you a structured checklist of questions to ask any broker before you deposit a single dollar. Use it properly and you will walk into any broker evaluation with more clarity than most retail traders ever develop.

The questions are organised by category, from regulation and fund safety through to fees, execution, and red flags. Each one surfaces something a broker's homepage almost certainly will not volunteer.

Why Most Traders Skip This Step (And Regret It)

Opening a trading account feels deceptively simple. You fill in a form, upload some ID, and click deposit. The problem surfaces later: spreads are twice what you expected, withdrawals take two weeks, or the regulator listed on the website turns out to be a Caribbean licensing body with no meaningful enforcement power.

By the time you find out, your capital is already inside.

Traders who avoid this outcome are not necessarily more experienced. They simply asked the right questions before committing funds. That is what this checklist is for.

Regulation and Licensing

Your money's first line of defence is the regulatory body overseeing it.

Which regulator oversees this broker?

Every legitimate broker is regulated somewhere. The question is where, and by whom. Regulators vary considerably in how much protection they actually provide.

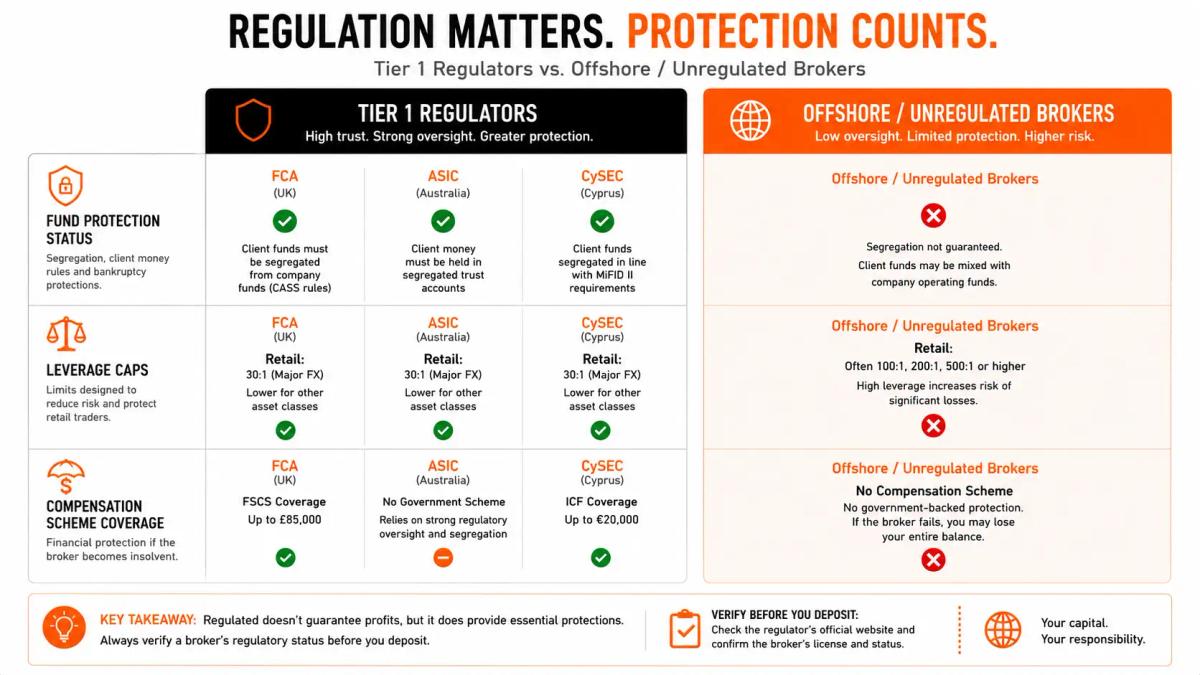

Tier 1 regulators are the ones that matter most for retail traders:

- FCA - Financial Conduct Authority (United Kingdom)

- ASIC - Australian Securities and Investments Commission (Australia)

- CySEC - Cyprus Securities and Exchange Commission (European Union)

- CFTC / NFA - Commodity Futures Trading Commission and National Futures Association (United States). The CFTC is the primary government regulator for retail forex and derivatives; the NFA is the self-regulatory body operating under its oversight. FINRA, while a significant financial regulator in the US, has limited scope in retail forex and derivatives specifically.

These bodies enforce capital adequacy requirements, conduct regular audits, and carry real enforcement power. Brokers regulated by them operate under meaningful constraints.

Offshore regulators, by contrast, often require little more than a registration fee. Jurisdictions like Vanuatu, the Seychelles, or St Vincent and the Grenadines are common homes for brokers seeking minimal oversight. That means you are accepting meaningfully more risk with less recourse if something goes wrong.

To verify a broker's licence, go directly to the regulator's official website and search the firm register. Do not rely on a licence number displayed on the broker's own site.

Does that regulator actually protect my funds?

Regulation and protection are not the same thing. A regulator sets standards and can act against rule-breaking brokers, but it cannot guarantee you will recover your money if a broker fails.

What matters beyond regulation is whether the broker's jurisdiction includes an investor compensation scheme, and what that scheme actually covers. That question leads directly to the next section.

Fund Safety and Segregation

Regulation tells you who is watching the broker. Fund safety tells you what happens to your money if the broker stops operating.

Are client funds held in segregated accounts?

Segregated accounts means the broker holds your funds separately from its own operating capital. If the broker becomes insolvent, client funds are ring-fenced and cannot be used to pay the broker's creditors.

This is a non-negotiable requirement for brokers regulated by Tier 1 bodies. If it is not explicitly stated, ask for written confirmation and look for it in the legal documentation rather than the marketing copy.

Is there investor compensation scheme coverage?

Some jurisdictions offer formal compensation schemes that pay out to retail clients if a regulated broker collapses. Two of the most relevant examples:

- FSCS - Financial Services Compensation Scheme (UK): for investment firm failures (which covers broker insolvency), eligible claimants are protected up to £85,000 per firm. Note that the separate FSCS deposit protection limit, which applies to bank and building society deposits rather than investment firms, is different. Confirm which limit applies to your specific account type at the time of your evaluation.

- ICF - Investor Compensation Fund (Cyprus/CySEC): covers eligible claimants up to €20,000 per person

These schemes cover firm failure, not trading losses. If you lose money trading, no compensation scheme covers that. These protections exist only for the scenario where the broker itself defaults or becomes insolvent.

Check whether you qualify as an eligible claimant under the relevant scheme. Compensation rules often exclude professional clients or non-residents.

Fees, Spreads, and Hidden Costs

This is where traders most often get surprised, and almost always in the wrong direction.

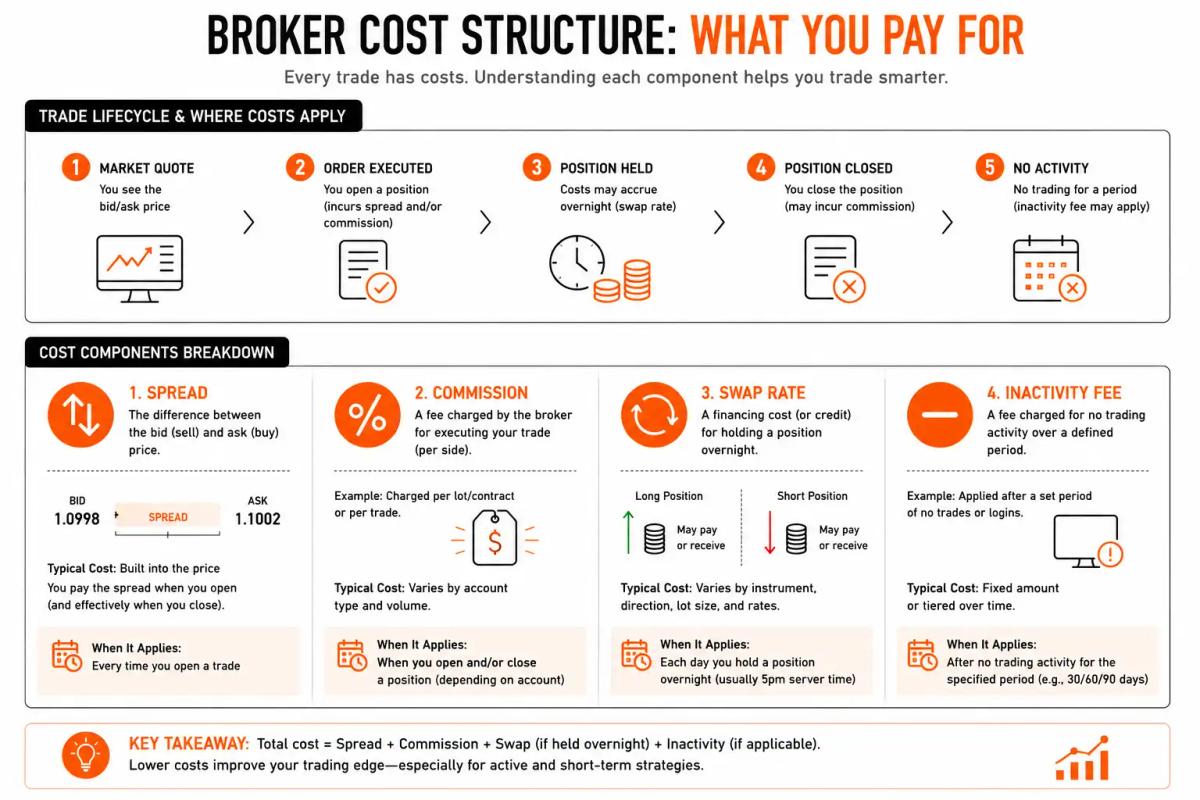

What are the actual spreads on instruments I trade?

A spread is the difference between the buy price and the sell price of an instrument. It is the most immediate cost of every trade you place. Brokers often advertise their tightest spreads (sometimes "from 0.0 pips"), which tend to apply only to premium account tiers or during peak liquidity hours.

Before opening an account, check the typical spreads on the specific instruments you plan to trade, during the hours you plan to trade them. A spread that looks competitive on EUR/USD at 9am London time can look very different at 11pm.

Are there inactivity fees, withdrawal fees, or deposit fees?

The spread is not the only cost. Run through this list when evaluating any broker:

- Inactivity fees: charged after a set period of no trading (often 3-12 months). Even small monthly charges erode dormant accounts steadily.

- Withdrawal fees: some brokers charge per withdrawal or impose minimum withdrawal amounts.

- Deposit fees: less common, but worth checking for specific payment methods.

- Currency conversion fees: if your account currency differs from your deposit currency, conversion spreads apply.

- Swap rates: the overnight financing cost for holding leveraged positions past the daily rollover. These can be positive or negative depending on direction and instrument, and they accumulate on positions held for days or weeks.

How is the broker compensated: spread markup or commission?

This tells you how the broker makes money, which reveals a lot about potential conflicts of interest.

- Spread markup: the broker widens the interbank spread before passing it to you. No explicit commission charge, but the cost is built into every trade.

- Commission model: tighter raw spreads with a fixed commission per lot or per trade. Common in ECN-style accounts.

Neither model is inherently better for the trader. What matters is the total cost per trade across the instruments you trade most. Calculate it both ways before deciding.

Leverage and Jurisdiction Rules

Leverage can amplify returns and losses in equal measure. The amount available to you is often determined by where you live.

What leverage is available in my country?

In the UK and EU, retail clients are subject to leverage caps under FCA and ESMA rules. On major forex pairs the cap is 30:1, falling to 20:1 on minor pairs and 10:1 on commodities and indices. UK retail clients face an additional restriction on cryptocurrency: the FCA has banned the sale of crypto-asset derivatives and exchange-traded notes to retail consumers entirely, meaning crypto leverage products are not available from FCA-regulated brokers to UK retail clients regardless of leverage level. EU rules under ESMA apply a 2:1 cap on crypto derivatives for retail clients, though individual member state regulators may apply stricter measures.

Traders outside these jurisdictions may find brokers offering leverage of 100:1, 200:1, or higher. This reflects genuinely different regulatory rules in different markets.

Why does leverage differ by jurisdiction?

Regulators in the UK and EU determined that high leverage presented too much risk to retail traders and set caps accordingly. Other regulators reached different conclusions. Neither position means offshore brokers are automatically reckless, but it does mean you need to understand which rules apply to you, based on your country of residence and the broker's licensing jurisdiction.

Before using any leverage level, understand what it means for your required margin and your potential loss on a position.

Platform and Execution

The platform is where you spend your time as a trader. The execution model determines whether your broker is working alongside you or across the trade from you.

Which trading platforms are supported?

The three most widely used retail trading platforms are:

- MetaTrader 4 (MT4): the industry standard for forex retail trading, with an extensive third-party tool ecosystem.

- MetaTrader 5 (MT5): MT4's successor, with broader asset class support and additional order types.

- cTrader: popular in ECN environments, with a clean interface and depth-of-market transparency that many traders prefer.

Check whether the broker's platform is available on the devices you use, whether a desktop or browser-based version is available, and whether the mobile apps are functional enough for your needs.

What execution model does the broker use: STP, ECN, or market maker?

This is one of the most practically important questions on this list.

- STP (Straight-Through Processing): your order is passed directly to a liquidity provider with no dealer intervention. The broker earns on the spread markup.

- ECN (Electronic Communications Network): your order goes into a network where it can be matched with other participants. Typically tighter spreads with a commission, and more pricing transparency.

- Market maker: the broker takes the other side of your trade. They benefit when you lose. This creates a structural conflict of interest. Understanding the dynamic before you deposit is worth the two minutes it takes.

Some brokers operate a hybrid model depending on account type. Ask directly, and confirm it in the legal documentation.

Account Types and Minimum Deposits

Not every account type suits every trader. Understanding the options before you deposit prevents you from starting on the wrong tier.

What account types are available and what do they require?

Most brokers offer tiered accounts, typically structured something like this:

The right account depends on your trading style and frequency. High-volume traders often benefit from lower spreads with commissions. Occasional traders may find a simpler spread-based structure easier to manage.

Can I start on a demo account before funding?

A demo account lets you test the platform, observe spreads under live conditions, and evaluate order execution before any real capital is at risk. Any broker worth considering should offer one.

Use the demo account actively. Place trades during the hours you plan to trade live, watch how spreads behave, and evaluate platform performance under different conditions. A demo is not a perfect replica of live trading, but it tells you considerably more than a broker's marketing page ever will.

Withdrawals and Deposit Methods

How easily you can get your money out matters as much as how easily you can put it in.

How long do withdrawals take and what methods are available?

Standard withdrawal timeframes vary by method:

- Bank wire transfers: typically 3-5 business days

- Credit/debit card: typically 2-5 business days

- E-wallets (Skrill, Neteller, PayPal): often 24-48 hours

Check whether the broker's stated timelines match what independent user reviews report. A consistent gap between the two is informative.

Also confirm which deposit methods are accepted and whether the same methods are available for withdrawals. Some brokers accept deposits via credit card but only process withdrawals by bank transfer, which changes the practical timeline considerably.

Are there withdrawal restrictions or conditions?

Read the withdrawal terms carefully. Conditions worth scrutinising include:

- Minimum withdrawal amounts

- Requirements to withdraw via the same method used to deposit

- Conditions attached to bonuses that restrict withdrawals until a trading volume target is met

- Documentation requirements beyond standard identity verification

If a broker's withdrawal terms are difficult to find, treat that as a data point in itself. Transparent brokers publish their terms clearly. How you manage capital across positions is a related consideration; the risk management and position sizing guide covers that in more detail.

Customer Support

Good support is invisible when everything works. It matters enormously when something goes wrong.

What support channels are available and when?

Check specifically:

- Live chat, email, and phone availability

- Trading hours coverage versus 24/5 or 24/7 availability

- Average response times (look for independent reports, not the broker's own claims)

Support available only by email during business hours in one time zone is a real constraint if you trade outside those hours.

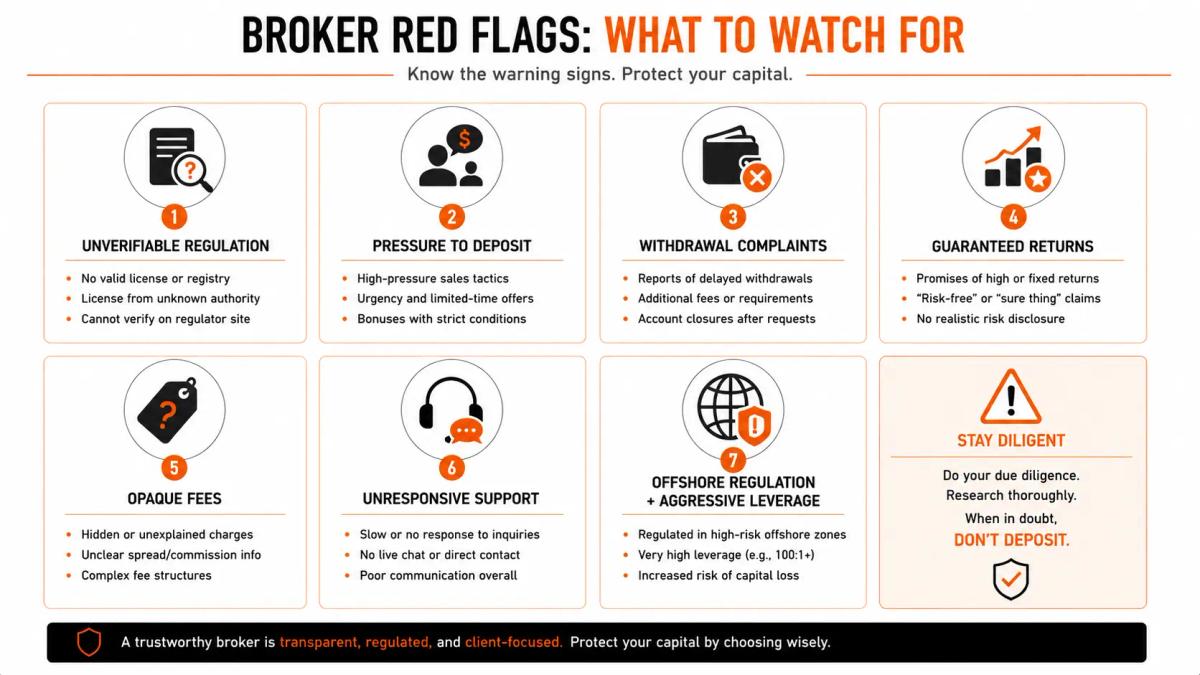

Red Flags to Watch For Before You Sign Up

Most broker problems leave visible traces before you deposit. Here is what to look for:

- Unverifiable regulation: the licence number does not appear in the official regulator's register, or the named regulator is not independently searchable.

- Pressure to deposit quickly: urgency framing around deposit deadlines, time-limited offers, or bonus expiry is a manipulation tactic, not a genuine offer.

- Withdrawal complaints: search the broker name alongside "withdrawal problems" or "withdrawal refused" on independent forums and review platforms. A pattern of complaints is a serious warning.

- Guaranteed returns: no legitimate broker guarantees trading profits. Any that does is misrepresenting the nature of trading.

- Opaque fee structures: if you cannot find the full fee schedule in the legal documentation before opening an account, assume the costs are structured to your disadvantage.

- Unresponsive pre-sales support: if support is hard to reach before you deposit, it will not improve once you have.

- Offshore regulation plus aggressive leverage offers: neither offshore regulation nor high leverage is automatically disqualifying, but the combination of both with high-pressure marketing is a recognisable pattern worth taking seriously.

Your Pre-Account Checklist (Summary)

Before you open any trading account, confirm you can answer yes to each of these:

Regulation

- [ ] I have verified the broker's licence directly on the regulator's official website

- [ ] The regulator is a Tier 1 body, or I understand the elevated risk of the alternative

Fund Safety

- [ ] Client funds are held in segregated accounts (confirmed in legal documentation)

- [ ] I know whether investor compensation scheme coverage applies to me and at what limit

Fees

- [ ] I know the typical spreads on the instruments I plan to trade

- [ ] I have checked for inactivity fees, withdrawal fees, and deposit fees

- [ ] I understand how the broker is compensated and what that means for total trade cost

Leverage

- [ ] I know what leverage is available to me under the rules that apply to my jurisdiction

Platform and Execution

- [ ] I have tested the platform on a demo account

- [ ] I know the broker's execution model (STP, ECN, or market maker)

Withdrawals

- [ ] I know the withdrawal methods, timelines, and any conditions that apply

- [ ] I have checked independent reviews for withdrawal complaints

Red Flags

- [ ] I found no significant pattern of complaints or unresolvable red flags in independent sources

If you want to compare brokers already assessed against these criteria, the regulated broker comparison directory gives you a starting point without having to run every check from scratch. For more detailed breakdowns on specific firms, the individual broker reviews are a useful next step.

Frequently Asked Questions

What does the minimum deposit requirement tell me about a broker?

The minimum deposit itself is not a quality signal in either direction. Low minimums attract beginners, which some legitimate brokers actively target. What the minimum deposit tells you is which account tier you qualify for and what trading conditions apply at that level. A very low deposit may only access a standard account with wider spreads, rather than the ECN conditions advertised on the homepage.

Is a demo account enough to properly evaluate a broker before depositing?

A demo account is a necessary part of evaluation but not a complete one. It lets you test the platform, observe spreads, and practise execution without risk. It does not replicate slippage during volatile conditions or reveal how the broker handles real withdrawals. Use the demo account thoroughly, but combine it with regulatory verification and independent review research before committing real capital.

How do I verify a broker's regulatory licence independently?

Go directly to the official website of the regulator the broker claims to be licensed by. Every Tier 1 regulator maintains a public register of authorised firms. Search the broker's legal entity name (not necessarily its trading name) and confirm the licence number matches, that the licence is current, and that the permissions cover the services the broker offers. Do not rely on the licence number displayed on the broker's own website as your only check.

What do segregated funds actually mean in practice?

Segregation means the broker holds your money in a bank account that is legally separate from the broker's own operating funds. In the event of broker insolvency, your money cannot be claimed by the broker's creditors. In practice, this protection depends on the quality of the segregation arrangements and the jurisdiction's insolvency laws. Segregation reduces risk but does not eliminate it entirely, and it works best in combination with a robust regulatory framework.

Are offshore brokers ever a legitimate choice?

Some offshore brokers operate professionally and serve clients in jurisdictions where Tier 1 regulated brokers do not hold licences. The risk is elevated because regulatory oversight is weaker and recourse in a dispute is limited. If you are considering an offshore broker, proportionally more due diligence is required: greater focus on withdrawal track records, community reputation, and the depth of independent reviews available.

How do leverage limits differ between UK/EU traders and traders in other jurisdictions?

UK retail traders are subject to FCA leverage caps on forex and most other instruments, and face an outright ban on crypto-asset derivatives and exchange-traded notes from FCA-regulated brokers. EU retail traders under ESMA rules are subject to leverage caps by asset class, including a 2:1 cap on crypto derivatives, though individual member state regulators may apply stricter measures. On major forex pairs, both UK and EU retail clients are capped at 30:1. Traders outside these jurisdictions may find brokers offering substantially higher leverage under local rules. The leverage level available to you depends on your country of residence and the regulatory jurisdiction your broker operates under for your account. This is a factual difference in rules, not a recommendation for or against any specific leverage level.

What should I do if a broker delays or refuses a withdrawal?

Start by raising a formal complaint in writing through the broker's official complaints process, which creates a documented record. If the broker is regulated by a Tier 1 body, you can escalate to the regulator directly. In the UK, the Financial Ombudsman Service handles unresolved complaints against FCA-regulated firms. For offshore brokers, formal escalation options are more limited, which is one of the practical costs of reduced regulatory oversight. Document every communication and keep records of your account balance and transaction history throughout.

About the authors

Related articles

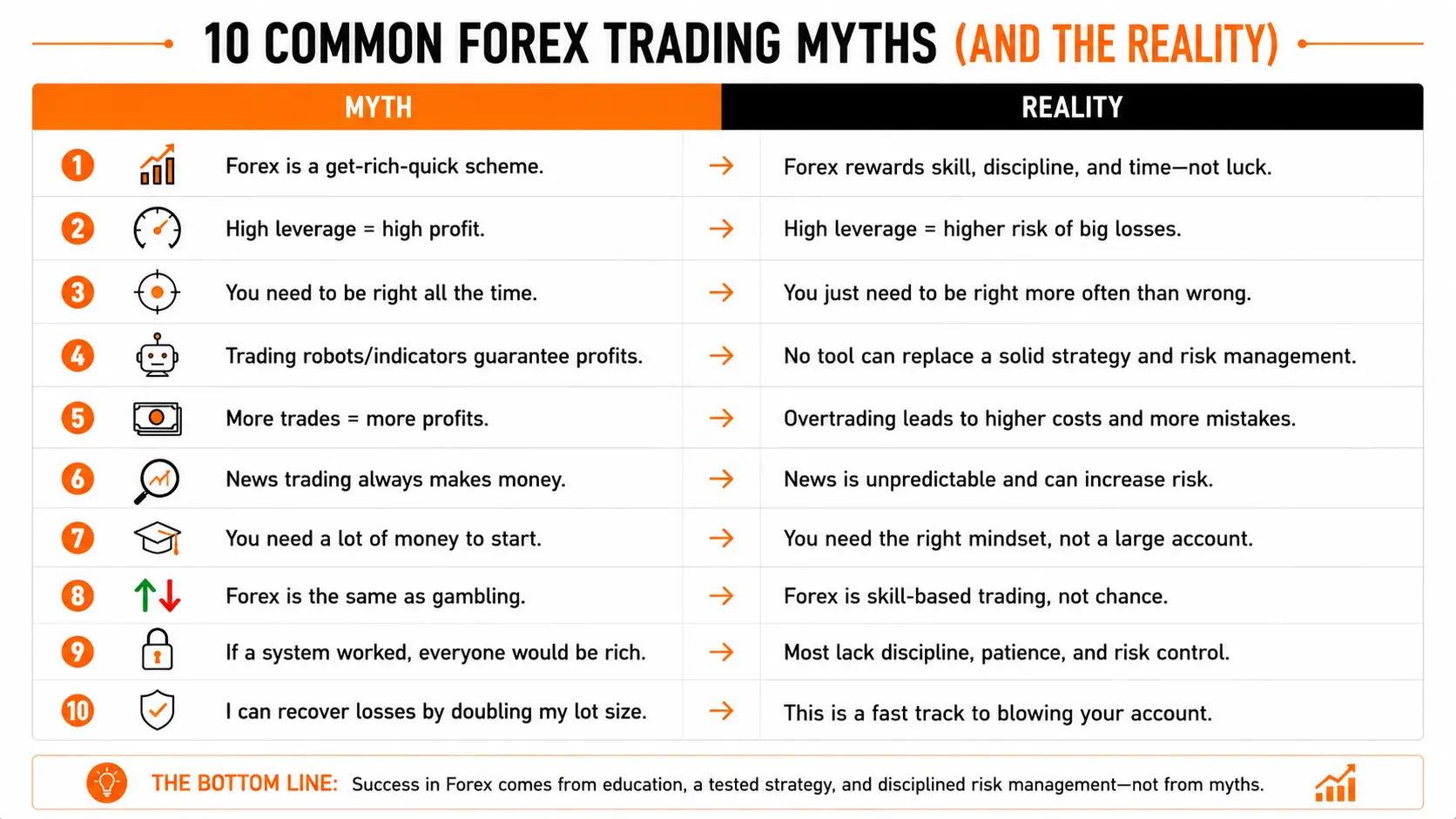

10 Forex Trading Myths That Are Costing You Money

From leverage to signal services, these 10 forex trading myths cost retail traders real money. Here's what the evidence actually shows.

What Is Fundamental Analysis? How Economic Data Moves Currency Markets

Learn how fundamental analysis works in forex: how interest rates, inflation, jobs, and GDP data move currencies, and how to read the economic calendar.

ECN vs Market Maker Broker: What the Difference Actually Costs You

ECN vs market maker broker: understand the real cost difference, conflict of interest risks, and which model suits your trading style

0 comments